Financial services are going through a transformative change. The industry is evolving from closed, single-vendor and proprietary systems to open, API-driven platforms focused on customer needs and integration ease. That change began with regulatory requirements such as PSD2 in Europe, Open Banking in the UK and the Consumer Data Right in Australia, but has now become far more than a matter of compliance.

Today, customer experience has become the primary battleground for financial institutions. Banks and fintech companies are no longer competing solely on rates or branch locations. Instead, they compete on how quickly they can open an account, how easily users can view all their finances in one place, and how well they anticipate customer needs. According to McKinsey research on digital banking transformation, banks that excel in customer experience grow revenues 3.2 times faster than their competitors and achieve cost-to-income ratios 20% lower than industry averages.

At the heart of this evolution, lies Open Banking API integration. It lets financial institutions share data securely, process payments quickly and develop services that can be used by multiple providers. For those organisational decision-makers that are looking to undertake digital transformation, gaining insight into how Open Banking is changing customer experience will no longer be a luxury. It is shaping which institutions will surge to the lead and which risk falling behind.

What Open Banking API Integration Actually Means

Open Banking represents a technical and business model where financial institutions expose their core services through standardized application programming interfaces. These APIs allow authorized third parties to access customer data and initiate actions, always with explicit customer consent.

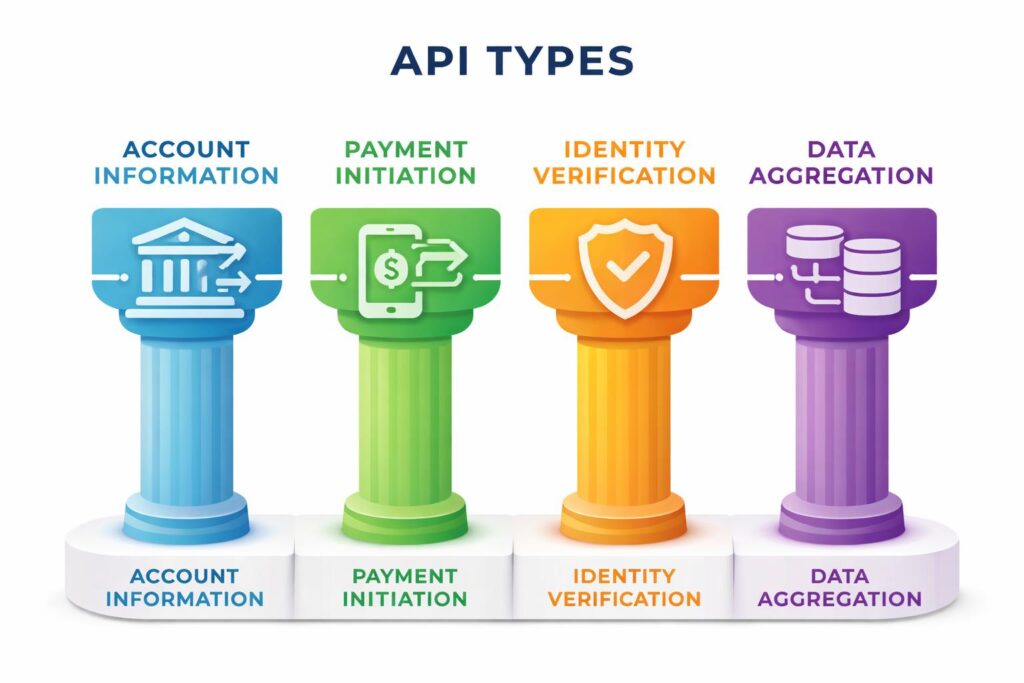

From a technical perspective, Open Banking APIs fall into several distinct categories, each serving specific functions and delivering unique customer experience improvements:

| API Type | Primary Function | CX Improvement | Business Value |

| Account Information | Retrieve balances, transactions, account details | Consolidated financial view, automatic data updates | Customer retention, engagement, cross-sell opportunities |

| Payment Initiation | Execute bank-to-bank transfers | Faster checkout, lower failure rates, no card entry | Reduced costs, higher conversion, instant settlement |

| Identity Verification | Confirm customer identity using banking data | Instant onboarding, reduced abandonment | Lower fraud, faster activation, better conversion |

| Data Aggregation | Combine information across multiple institutions | Complete financial picture, better insights | Personalization, risk assessment, product innovation |

The difference between traditional integrations and modern API-first models is significant. Traditional banking integrations required custom point-to-point connections, often taking months to establish and maintain. Each integration was unique, creating technical debt and limiting scalability. API-first approaches use standardized protocols, documented endpoints, and common authentication methods. This reduces integration time from months to weeks, sometimes days. It also enables a many-to-many ecosystem where one API integration opens connections to hundreds of financial institutions.

Why Customer Experience Is Becoming the Core Benefit

Open Banking started as a regulatory requirement designed to increase competition and give customers more control over their financial data. However, leading institutions quickly recognized its potential to transform customer experience from a compliance burden into a strategic differentiator.

Modern customers expect their banking experience to match what they get from other digital services. They want transparency about fees and spending patterns. They expect instant results when making payments or checking balances. They demand personalization that reflects their actual financial situation, not generic product offers. Traditional banking systems, built on batch processing and siloed data, cannot deliver these experiences efficiently.

Open Banking changes the foundation. When financial data flows freely between authorized systems through secure APIs, institutions can build experiences that were previously impossible. A mortgage application that used to require weeks of document gathering can now pull verified income and asset data in seconds. A business loan decision that once took days can happen in minutes using real-time cash flow analysis. A budgeting tool that required manual data entry now updates automatically across all accounts.

The shift from regulatory compliance to experience innovation happened because institutions realized that customers value convenience and insight more than they fear data sharing. When presented with clear benefits and proper security controls, customers willingly share financial data to get better services.

Key Ways Open Banking API Integration Is Reshaping Customer Experience

Hyper-personalized Financial Services

Open Banking APIs also allows a level of customisation not possible with legacy banking systems. With transaction information from multiple accounts and institutions, financial services can base their assessments on actual spending habits, income predictability and money behavior far more than static demographic data or credit scores can provide.

AI-powered personalization leverages this wealth of information to deliver context-aware recommendations. A budgeting app might recognize that a customer spends much more on eating out in some months than others and offer automated adjustments to savings. A wealth management platform can see cash sitting idle in checking accounts and suggest investment options that suit the profile and goals of its customer. A lending service could provide credit exactly when cash flow analysis suggests such support is needed by the customer, under terms tailored to their actual financial condition.

The key advantage comes from data aggregation. When APIs pull information from multiple banks, credit cards, and investment accounts, the resulting picture of customer finances is far more complete than what any single institution sees. This comprehensive view enables services that feel genuinely personalized rather than segment-based.

Seamless Onboarding and Identity Verification

Customer onboarding has historically been one of the most friction-heavy processes in financial services. Know Your Customer regulations require identity verification, address confirmation, and risk assessment. Traditional methods involve uploading documents, waiting for manual review, and dealing with rejection rates when documents are unclear or incomplete.

Open Banking APIs transform this process. Instead of uploading bank statements to prove income or address, customers can authorize direct access to their banking data. The verification happens instantly, with higher accuracy than manual document review. Identity verification APIs can confirm that the person opening an account matches verified banking records, reducing fraud risk while eliminating delays.

Technologies like OAuth 2.0 and OpenID Connect provide the security framework for this seamless verification. Customers authenticate once with their existing bank credentials, grant specific permissions, and the onboarding system receives only the necessary data. Biometric authentication adds another layer of security without adding friction. The result is onboarding that takes minutes instead of days, with conversion rates that can improve by 40-60% compared to traditional processes.

Faster, Frictionless Payments

Payment initiation with Open Banking APIs is a game changer compared to card payments. With traditional card transactions, there are multiple intermediaries that introduce additional cost and complexity. Open Banking allows for bank-to-bank transfers directly through APIs, bypassing these middlemen.

For consumers, this translates into real-time payment verification without having to input card information, reduced failure rates and greater security as the consumer’s sensitive payment data never enters the merchant environment. For merchants and service providers, that means lower transaction fees, instant settlement as well as lesser fraud risk.

E-commerce platforms benefit particularly from these improvements. Cart abandonment rates drop when checkout requires only authentication with a banking app instead of finding and entering card details. Subscription services see fewer failed payments when they use account-to-account transfers instead of card charges that expire or get blocked. Neobanks can offer peer-to-peer payments that settle instantly rather than taking days.

The business case is compelling. Payment initiation APIs can reduce transaction costs by 50-70% compared to card networks while providing faster settlement and better customer experience.

Consolidated Financial Dashboards and Multi-banking Experience

One of the most visible customer experience improvements from Open Banking is the ability to view and manage finances across multiple institutions in a single interface. Data aggregation APIs make this possible by pulling account information, transaction history, and balance data from different banks into unified dashboards.

This consolidation provides significant UX benefits. Instead of logging into five different banking apps to check balances, customers see everything in one place. Instead of manually categorizing spending across multiple cards, they get automatic analysis of total spending patterns. Instead of switching between apps to move money, they can initiate transfers between any connected accounts from a single interface.

The reduction in cognitive load and interaction friction is substantial. Research shows that customers who use consolidated financial dashboards engage with their finances more frequently and make better financial decisions. They spot unusual spending patterns faster, identify savings opportunities more easily, and maintain better awareness of their overall financial health.

For financial institutions, offering multi-banking experiences through Open Banking APIs creates stickiness. Even if a customer uses accounts from multiple banks, the institution providing the best aggregation and analysis interface becomes the primary touchpoint.

Proactive Risk Insights and Smarter Credit Decisions

Open Banking APIs enable more accurate risk assessment and credit decisions by providing access to real-time, verified financial data. Traditional credit scoring relies heavily on historical credit bureau data, which may be months out of date and tells an incomplete story. Open Banking allows lenders to analyze current account balances, income patterns, spending behaviors, and cash flow trends.

This shift has profound implications for customer experience. Credit decisions become faster and more accurate. Customers with thin credit files but stable banking histories can access credit products previously unavailable to them. Loan terms can be personalized based on actual financial capacity rather than broad risk categories. Businesses can get working capital based on real revenue data rather than lengthy application processes.

According to IEEE research on machine learning applications in financial services, lenders using Open Banking data for credit decisions see default rates drop by 15-25% while expanding their addressable market. The combination of better risk assessment and improved access creates a superior experience for both lenders and borrowers.

The proactive element comes from continuous monitoring. Instead of making a one-time credit decision, systems can monitor ongoing financial health and adjust credit limits, offer refinancing, or provide early warnings about potential cash flow problems. This transforms the lender-borrower relationship from transactional to advisory.

How Open Banking Enhances Product and Service Innovation

Open Banking API integration does more than improve existing services. It enables entirely new business models and product categories that were impractical or impossible with traditional banking infrastructure.

Embedded finance represents one of the most significant innovations. Non-financial companies can now integrate banking services directly into their platforms using Open Banking APIs. A property management platform can offer tenant screening based on verified banking data. An accounting system can provide instant business loans based on real-time revenue analysis. A ride-sharing app can offer instant driver payouts using payment initiation APIs.

BNPL lenders lean heavily on Open Banking for real-time credit assessment and account-to-account payment fulfilment. Apps that automatically save use transaction data to find loose change and shift it around into savings or investment accounts, depending on customer rules. Lending platforms that offer financing immediately (within minutes) with income and expenses data validated in Open Banking APIs.

These innovations share common characteristics. They deliver instant value, ask little from the user and slip nicely into existing workflows. Standardized APIs and a partner ecosystem create the conditions for that. Instead of white-labelling ten or twelve services to create a bank, a fintech startup can stitch together four or five well-designed APIs and obtain most of the building blocks it needs to deliver complex financial services.

Technical Foundations of Open Banking API Integration

Delivering excellent customer experience through Open Banking requires solid technical foundations. The architecture decisions made during implementation directly impact performance, security, and reliability, which customers feel as speed, safety, and trustworthiness. Building a successful Open Banking platform requires attention to several critical components:

API gateway with rate limiting and traffic management – This serves as the control point for all Open Banking interactions, handling authentication, routing requests to appropriate backend systems, managing rate limiting to prevent abuse, and providing monitoring and analytics.

OAuth 2.0 and OpenID Connect for secure authentication – These standards provide the security framework for seamless verification, allowing customers to authenticate once with their existing bank credentials and grant specific permissions.

Microservices-based backend for modularity and scalability – Individual services can be updated, scaled, or replaced without affecting others, enabling rapid feature deployment without full system releases.

Event-driven architecture for real-time processing – This allows real-time responses to financial activities, creating experiences that feel intelligent and attentive.

Cloud-native infrastructure for elastic scaling – Systems can automatically provision resources to handle load spikes during high-traffic periods, then scale back down to optimize costs.

Tokenization and encryption for data protection – Sensitive data is replaced with temporary tokens that have limited scope and lifespan, ensuring that even intercepted tokens cannot be reused beyond their specific authorized purpose.

Comprehensive logging and monitoring systems – These track real user experience metrics like time to interactive, API error rates by user journey, and conversion impact from performance issues.

Consent management interface for customer control – Well-designed consent interfaces clearly explain what access customers are granting, how long it will last, and how to revoke it.

API Gateways and Secure Access Layers

API gateways serve as the control point for all Open Banking interactions. They handle authentication, route requests to appropriate backend systems, manage rate limiting to prevent abuse, and provide monitoring and analytics. Well-designed gateways protect backend systems from overload while ensuring that legitimate requests receive fast responses.

Rate limiting and throttling are essential for maintaining service quality. They prevent any single consumer from monopolizing resources and protect against denial-of-service attacks. However, they must be calibrated carefully. Too restrictive, and legitimate high-volume use cases fail. Too permissive, and system stability suffers.

Traffic control mechanisms ensure that customer-facing requests get priority over background processes. During peak usage times, this prioritization keeps the customer experience responsive even when backend systems are under heavy load.

Data Standardization and Interoperability

The customer experience benefits of Open Banking depend on standardized data formats that work consistently across institutions. When every bank returns transaction data in the same structure, applications can process it reliably without custom code for each provider.

Open standards like ISO 20022 provide common schemas for financial messaging. These standards define how to represent payments, account information, and other financial data in machine-readable formats. Adoption of these standards reduces integration complexity and improves data quality.

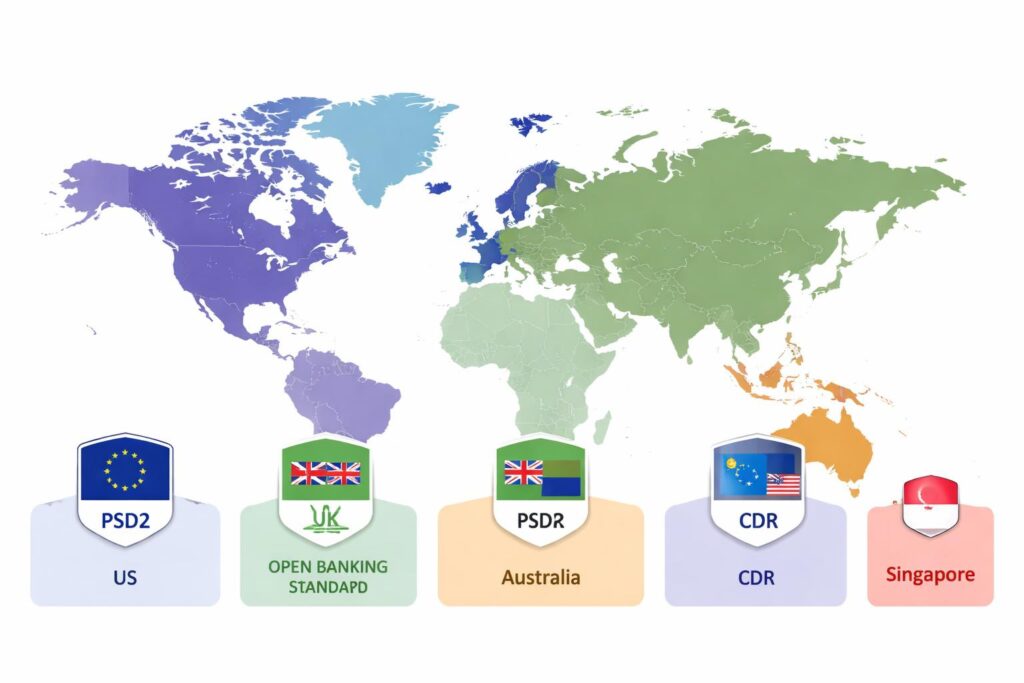

However, standardization remains incomplete across regions, as shown in this comparison of major Open Banking frameworks:

| Region | Regulatory Framework | Mandatory Timeline | Technical Standard | Coverage |

| European Union | PSD2 | 2018 mandatory | PSD2 API (varied by country) | Payment accounts, credit transfers |

| United Kingdom | Open Banking Standard | 2018 mandatory for major banks | Open Banking API v3.1+ | Current accounts, credit cards, savings |

| Australia | Consumer Data Right | 2020 banking, expanding | CDR API Standards | Banking, energy, telecom (phased) |

| United States | Voluntary adoption | No mandate | Proprietary + FDX emerging | Varies by institution |

| Singapore | API Playbook | Voluntary, encouraged | APIX standards recommended | Varies by bank |

This fragmentation creates challenges for platforms operating across multiple regions, requiring adaptation layers that can translate between standards.

Security and Consent Management

Security architecture determines whether customers trust Open Banking services enough to use them. Strong customer authentication requires at least two independent verification factors, such as something the customer knows (password), something they have (mobile device), and something they are (biometric).

Tokenization protects sensitive data by replacing actual account numbers and credentials with temporary tokens that have limited scope and lifespan. Even if intercepted, these tokens cannot be reused beyond their specific authorized purpose.

Consent management systems give customers granular control over what data they share and with whom. Well-designed consent interfaces clearly explain what access they are granting, how long it will last, and how to revoke it. Transparency in consent management builds trust, while confusing or overly broad consent requests create friction and abandonment.

Data minimization principles ensure that APIs only expose the specific data needed for the requested service, nothing more. This reduces privacy risk and regulatory exposure while improving customer confidence.

Cloud-native Architecture and Microservices

Modern Open Banking implementations use cloud-native architectures built on microservices rather than monolithic applications. This modularity provides several customer experience benefits. Individual services can be updated, scaled, or replaced without affecting others. New features can be deployed rapidly without full system releases. Failures in one component do not cascade through the entire system.

Event-driven models allow real-time responses to financial activities. When a large purchase occurs, an event can trigger fraud analysis, budget alerts, and reward calculations simultaneously. This responsiveness creates experiences that feel intelligent and attentive.

Scalability ensures that customer experience does not degrade during high-traffic periods. Cloud-native systems can automatically provision resources to handle load spikes during events like Black Friday or tax deadlines, then scale back down to optimize costs.

Challenges Financial Companies Face with Open Banking Integration

Despite the clear benefits, implementing Open Banking API integration presents significant challenges that can impact project timelines, costs, and ultimate success.

Legacy Infrastructure Constraints

Most established financial institutions run on core banking systems that were designed decades ago. These legacy systems were built for batch processing, not real-time API interactions. They use proprietary data formats, not standardized schemas. They run on mainframes, not cloud infrastructure.

Connecting these legacy systems to modern Open Banking APIs requires middleware layers that translate between old and new architectures. This translation adds latency, creates potential failure points, and requires ongoing maintenance. In some cases, core system limitations make certain Open Banking use cases impractical without fundamental infrastructure modernization.

The integration complexity can be severe. A single account balance request through an Open Banking API might trigger queries across multiple legacy systems, each with different response times and data formats. Ensuring consistency and performance across these distributed calls requires sophisticated orchestration.

Data Privacy and Security Risks

Customers worry about sharing financial data, even when they understand the benefits. High-profile data breaches at major institutions have made people cautious. Regulatory requirements like GDPR add complexity to how data can be stored, processed, and shared.

Financial institutions face liability concerns. If customer data is compromised through an Open Banking API, who bears responsibility? The bank that exposed the API, the third party that consumed it, or the technology providers in between? These questions are still being resolved in courts and regulatory frameworks.

Security risks extend beyond data breaches. API vulnerabilities can be exploited for fraud, unauthorized transactions, or system disruption. Maintaining security requires constant vigilance, regular penetration testing, and rapid response to newly discovered vulnerabilities.

Fragmented Standards Across Regions

Open Banking has developed differently in various parts of the world, creating a patchwork of incompatible standards. European PSD2 regulations mandate certain API capabilities but leave implementation details to national regulators. The UK Open Banking standard is more prescriptive but only applies within that market. The United States has no comprehensive Open Banking regulation, leading to proprietary approaches from different institutions. Asia-Pacific markets each have unique frameworks.

For companies operating globally, this fragmentation means maintaining multiple integration approaches, compliance frameworks, and technical implementations. A payment service that works seamlessly in London might require complete re-architecture to operate in Singapore or New York.

Standardization efforts are underway through organizations like the Financial Data Exchange, but achieving global consistency remains years away. Until then, companies must navigate regional differences carefully.

Vendor and Partner Coordination

Open Banking ecosystems involve multiple parties: the financial institution, third-party providers, technology vendors, API gateway operators, and sometimes regulatory technology providers. Coordinating these stakeholders presents project management challenges.

Integration requires agreement on technical specifications, security protocols, testing procedures, and operational responsibilities. When issues arise in production, determining which party should resolve them can create delays that impact customer experience. Service level agreements must clearly define responsibilities, but enforcing them across organizational boundaries is complex.

Vendor lock-in is another concern. Choosing a specific API gateway platform or integration provider can create long-term dependency. Switching costs can be high if the vendor relationship sours or if better alternatives emerge.

Best Practices for Delivering Exceptional Customer Experience Through Open Banking

Success in Open Banking requires more than technical implementation. It demands a strategic approach that keeps customer experience at the center of every decision. Organizations that excel in Open Banking customer experience typically focus on several critical success factors:

Clear value proposition communicated before data sharing – Customers need to understand exactly what they get in return for sharing their financial data. Vague promises of “better service” do not motivate consent. Specific benefits like instant loan approval, automated savings, or unified financial views drive adoption.

Transparent consent process with granular controls – Well-designed consent interfaces clearly explain what access customers are granting, how long it will last, and how to revoke it. Customers should be able to grant access to specific accounts or data types rather than all-or-nothing permissions.

Fast API response times (under 500ms target) – API performance directly impacts customer experience. A 500-millisecond delay in account balance retrieval might seem trivial in technical terms, but it creates noticeable lag in user interfaces.

Consistent experience across mobile, web, and other channels – Customers interact with financial services across mobile apps, web browsers, and sometimes physical devices. Open Banking experiences must maintain consistency across all these touchpoints.

Proactive error handling and customer communication – When API calls fail or data is temporarily unavailable, customers need clear explanations and guidance. Generic error messages create frustration and abandonment.

Regular security audits and compliance reviews – Security architecture determines whether customers trust Open Banking services enough to use them. Maintaining this trust requires constant vigilance.

Continuous performance monitoring and optimization – Monitoring and observability tools should track real user experience metrics, not just system performance.

Designing Data-centric User Journeys

The best Open Banking experiences start with understanding what customers actually need, then designing journeys that deliver those outcomes with minimal friction. This means moving beyond traditional product-centric thinking to data-centric design.

Instead of asking “How do we add Open Banking to our mobile app?”, effective teams ask “What financial problems do our customers face that access to their banking data could solve?” The answers might point to completely different features than initially imagined.

User journey mapping should identify every point where Open Banking data can reduce effort, provide insight, or enable new capabilities. A mortgage application journey might use Open Banking data for income verification, affordability assessment, deposit source confirmation, and ongoing payment management. Each touchpoint should feel seamless and valuable, not like data collection for its own sake.

Ensuring UX Consistency Across Platforms

Customers interact with financial services across mobile apps, web browsers, and sometimes physical devices. Open Banking experiences must maintain consistency across all these touchpoints while adapting appropriately to each platform’s capabilities and constraints.

Unified UI logic ensures that business rules, data presentations, and interaction patterns work the same way regardless of platform. A customer who starts connecting bank accounts on their desktop should be able to complete the process on their phone without confusion or repeated steps.

Responsive design goes beyond screen size adaptation. It considers network conditions, input methods, and usage contexts. Mobile users might be connecting accounts while commuting with unreliable connectivity. Desktop users might be making complex financial decisions that require detailed data visualization.

Session continuity allows customers to move seamlessly between devices without losing context. If a customer starts a loan application on mobile but needs to review detailed terms on a larger screen, their progress should carry over instantly.

Investing in API Performance and Reliability

API performance directly impacts customer experience. A 500-millisecond delay in account balance retrieval might seem trivial in technical terms, but it creates noticeable lag in user interfaces. Multiply that across multiple API calls in a single user journey, and the experience feels sluggish.

High-performing APIs require attention to multiple factors. Backend system optimization ensures fast data retrieval. Caching strategies reduce redundant calls to core banking systems. Connection pooling minimizes network overhead. Geographic distribution puts API endpoints close to users, reducing latency.

Reliability matters as much as speed. An API that responds in 100 milliseconds 95% of the time but fails 5% of the time creates worse customer experience than one that consistently responds in 200 milliseconds. Customers encountering failed connections lose trust quickly.

Monitoring and observability tools should track real user experience metrics, not just system performance. Time to interactive, API error rates by user journey, and conversion impact from performance issues provide better insights than server CPU utilization.

Choosing the Right Technology Partner

Few financial institutions build Open Banking capabilities entirely in-house. Strategic technology partnerships accelerate time to market and bring specialized expertise. However, choosing the wrong partner can create more problems than it solves.

Evaluation criteria should include demonstrated experience in financial services, not just general software development. Financial technology has unique requirements around security, compliance, transaction integrity, and regulatory reporting. Partners without deep fintech experience will face a steep learning curve on critical issues.

API integration capabilities should be evaluated through practical assessments. Can they demonstrate successful integrations with major banking platforms? Do they understand the nuances of different Open Banking standards across regions? Have they built systems that scale to handle millions of API calls?

Data security practices require thorough vetting. Partners should have demonstrated compliance with relevant standards like PCI DSS, ISO 27001, and region-specific requirements. They should understand tokenization, encryption at rest and in transit, and secure key management. Security should be built into their development process, not added later.

Cloud-native architecture expertise ensures that the solution can scale, recover from failures, and deploy updates without disruption. Partners building on legacy architectures will struggle to deliver the performance and agility that modern Open Banking requires.

Real-world Case Observations

Case 1: Digital Bank Account Aggregation

A European neobank wanted to differentiate itself by offering customers a complete view of their finances across multiple traditional banks. The problem was that manual account linking had less than 30% completion rates. Customers started the process but abandoned when faced with multiple login screens and security questions.

The API integration process involved implementing Open Banking account information APIs from major European banks, building an OAuth-based consent flow that clearly explained data usage, and designing a mobile-first interface that showed aggregated balances and transactions in real-time.

Results showed account linking completion rates increased to 78%. Customer engagement measured by monthly active users improved by 43% because users could see all their finances in one place. Retention after six months improved by 31% compared to users who did not link external accounts. The competitive advantage from multi-banking capability became a primary customer acquisition driver.

Case 2: Instant Payment Platform for E-commerce

A payment service provider serving mid-sized e-commerce merchants faced high cart abandonment rates and transaction costs from card processing. They needed a faster, cheaper payment method that would work across multiple countries.

The integration involved implementing payment initiation APIs following PSD2 standards, building a checkout experience that redirected customers to their banking app for authorization, and creating merchant dashboards showing instant settlement status.

Conversion rates at checkout improved by 22% because customers could complete purchases with just their banking credentials instead of finding and entering card details. Transaction costs decreased by 58% compared to card processing. Merchants reported 40% faster settlement, improving their cash flow. The success led to rapid merchant adoption across seven European markets.

Case 3: Wealth Management Onboarding

A wealth management platform struggled with onboarding friction. Customers needed to prove asset ownership and income levels through document uploads, which took an average of 11 days to verify manually. This delay caused 35% of started applications to be abandoned.

The solution used Open Banking APIs for instant verification of bank balances, investment accounts, and income through transaction analysis. The verification system analyzed three months of banking data to confirm income stability and asset levels, providing approval decisions in under 10 minutes.

Account opening time dropped from 11 days to same-day completion. Verification accuracy improved because banking data is harder to falsify than uploaded documents. Application abandonment fell from 35% to 8%. The platform could onboard customers during initial interest rather than losing them during multi-day verification processes.

Conclusion

Open Banking API integration has fundamentally changed what customers expect from financial services and how institutions deliver value. The shift from closed, proprietary systems to open, interoperable ecosystems has created opportunities to reimagine every aspect of the customer experience. Personalization, speed, transparency, and convenience have moved from differentiators to baseline expectations.

For financial institutions and fintech companies, Open Banking is no longer about regulatory compliance. It has become the foundation for competitive advantage in an increasingly digital market. Organizations that master API-first architectures, secure data sharing, and customer-centric design will define the next generation of financial services. Those that treat Open Banking as a technical checkbox will find themselves unable to compete on the experiences that customers now demand. The question is not whether to invest in Open Banking capabilities, but how quickly organizations can transform their infrastructure, processes, and culture to succeed in this new reality.

Ready to Transform Your Financial Services?

Open Banking integration requires deep expertise in API development, financial services architecture, and customer experience design. Our team helps financial institutions and fintech companies build secure, scalable Open Banking solutions that drive measurable improvements in customer satisfaction and business outcomes.

We provide end-to-end support for Open Banking initiatives, from compliance and API-first architecture to cloud engineering and customer experience optimization. Our proven approach has helped clients reduce onboarding time by 85%, improve payment conversion by over 40%, and create new revenue streams through embedded financial services.

Contact us to discuss how we can accelerate your Open Banking transformation.