Banks and financial institutions are making a major shift — and it’s not just about throwing a bunch of new features into their apps. The change runs deeper still. These companies are the types of businesses that are reimagining how they do business and AI is at the heart of it.

Consider what customers are expecting today. They seek things like instant decisions on loans, fraud alerts before they even know their money was at risk and financial advice that recognizes their own quirky situation. And regulators are pressuring for more transparency, faster reporting and better risk management. Competitors, particularly some of the newer fintechs, are already harnessing AI to move more quickly and serve customers better. Traditional organizations have been coming to the realization that they can no longer simply test AI with small projects. They should bake it into all they do.

According to McKinsey research, financial institutions that successfully integrate AI across their operations could add significant value annually. But here’s the challenge: most banks have spent years running pilot programs and experiments that never make it beyond the testing phase. They build impressive AI models that work beautifully in isolation but fail when they try to connect them to the messy reality of existing systems.

This is exactly why AI integration services have become so valuable. The real work isn’t building the AI. It’s making it work inside organizations that have decades of legacy technology, strict compliance requirements, and operations that can’t afford downtime. The institutions investing heavily in AI integration today aren’t chasing trends. They’re responding to a simple reality: adapt your technology to support intelligent operations, or watch your competitive position erode.

What AI Integration Services Actually Mean for Financial Institutions

Let’s clear up some confusion. Building an AI model and integrating AI into your operations are completely different challenges.

Building a model means teaching an algorithm to detect fraud or assess credit risk. Integration means getting that model to actually work inside a bank that has 30-year-old mainframe systems, compliance rules that can’t be violated, and millions of customers whose transactions can’t be disrupted.

The Core Components of AI Integration

AI integration services handle several interconnected layers:

Data Layer: Building unified pipelines that collect information from disparate sources—core banking systems, transaction processors, CRM platforms, external data providers—and transform it into formats AI models can consume.

Deployment Layer: Containerizing models, establishing API endpoints, implementing version control, and building monitoring systems that track performance and detect degradation.

Orchestration Layer: Managing how multiple AI models work together, with outputs from one serving as inputs to another, requiring careful sequencing and error handling.

Governance Layer: Establishing frameworks that document model logic, create audit trails for regulators, implement fallback mechanisms, and ensure appropriate security controls.

Here’s what makes financial services particularly complicated: nothing can break. A retail company can test new AI features on a small group of customers and roll back if something goes wrong. Banks can’t do that. When you’re processing loan applications or monitoring for money laundering, the systems have to work correctly every single time.

The Real Difference: Scratch vs. Integration

| Building From Scratch | Integrating into Existing Systems |

| Clean slate architecture | Must work with 20-40 year old legacy systems |

| Design optimal data flows | Navigate fragmented data across dozens of systems |

| Choose ideal technology stack | Bridge incompatible technologies and protocols |

| Set your own timelines | Maintain zero-downtime during deployment |

| Control all dependencies | Coordinate with multiple stakeholder teams |

The difference between building from scratch and integrating matters enormously. A bank that’s been around for decades has technology infrastructure layered like geological strata. Some of it is ancient but still handles critical functions that can’t simply be replaced. Integration services provide the connective tissue that lets AI enhance these systems without requiring a complete overhaul, which would cost hundreds of millions and create unacceptable risk.

Key Drivers Behind Growing Investments in AI Integration

Rising Operational Complexity

Banks today handle an overwhelming amount of work. A typical mid-sized institution processes millions of transactions every day across mobile apps, websites, branches, and ATMs. Each transaction generates data that needs recording, checking, and analysis.

Consider what happens behind a simple customer request:

A customer asks about a declined transaction through the mobile app. The AI system needs to: access transaction history from the payment processor, check fraud detection flags, review account status from the core banking system, examine recent customer communication from the CRM, analyze the merchant details from external databases, and generate a response that complies with disclosure requirements.

For a long time, banks managed complexity with large teams and rule-based software. But that approach stopped working as operations grew. The cost of hiring enough staff to manually review everything became unsustainable. More importantly, manual processes created delays and inconsistencies that frustrated customers and introduced risk.

The numbers tell the story: According to Deloitte’s research on AI in banking, financial institutions using AI for operational processes report reducing processing time by 50-70% while cutting error rates by up to 90%.

AI integration solves this by automating routine decisions and flagging the exceptions that actually need human judgment. A well-integrated AI system can process standard transactions straight through without any manual review, letting staff focus on complex cases that require expertise.

Regulatory Pressure and Compliance Automation

Regulatory requirements have exploded in complexity. The web of rules financial institutions must navigate now includes:

- AML/KYC: Anti-money laundering and Know Your Customer protocols requiring transaction monitoring across jurisdictions

- Basel III: Capital requirements demanding sophisticated risk modeling and stress testing

- GDPR: Data protection rules affecting how customer information gets collected, stored, and used

- PSD2: Payment services directive reshaping European payment infrastructure

- FATF: Financial Action Task Force guidelines on combating financial crimes

- Dodd-Frank: Comprehensive financial reform affecting US institutions

- MiFID II: Market regulation impacting investment services across Europe

Meeting these requirements manually is essentially impossible at scale. A compliance team can’t review every transaction for suspicious patterns when they’re dealing with millions of transactions daily.

How AI Integration Changes Compliance

Before AI Integration: Compliance teams manually review flagged transactions → Days or weeks of backlog develop → High false positive rates waste investigator time → Regulatory reports compiled manually from multiple systems → Constant struggle to keep pace with new requirements

After AI Integration: Real-time transaction monitoring across all channels → Automated pattern recognition identifies genuine risks → False positives reduced by 60-80% → Regulatory reports generated automatically with full audit trails → Models update as regulations change without manual reprogramming

For heavily regulated institutions, the return on investment in AI integration often comes primarily from compliance efficiency rather than revenue growth. When IBM studied financial compliance costs, they found that institutions spend an average of $270 million annually on compliance, with much of that going to manual processes that AI could automate.

Data as a Competitive Advantage

Every bank sits on enormous amounts of data about transactions, customer behavior, market conditions, and risk patterns. For years, this data mostly just accumulated in various systems without being used strategically. That’s changing rapidly because the institutions that can actually analyze and act on their data have a significant competitive edge.

Three Ways Data Creates Advantage:

Real-time decisioning: Spot opportunities and risks as they emerge rather than discovering them weeks later in reports. A customer’s transaction pattern might indicate they’re ready for a mortgage, but only if you can analyze that pattern and act on it immediately.

Predictive accuracy: Traditional credit scoring might use 15-20 variables. AI-powered scoring can incorporate hundreds of behavioral signals, transaction patterns, and external data points to assess risk more precisely. This lets institutions profitably serve customers that traditional models would reject.

Personalization at scale: Understanding individual customer needs across millions of relationships used to be impossible. AI integration makes it feasible by analyzing behavior patterns, life events, and financial trajectories to deliver relevant recommendations to each customer.

But here’s the thing: none of this happens unless the AI models are properly integrated into operational systems. A predictive model that identifies high-value customers is useless if that information never reaches the relationship managers who could act on it. The value of data-driven decision making depends entirely on integration quality.

Customer Experience Transformation

Customer expectations have moved far beyond basic digital access. Research from Accenture on banking customer expectations shows that 73% of customers expect companies to understand their unique needs and expectations, while 68% are willing to share personal data if it leads to more personalized experiences.

What Modern Banking Customers Actually Expect

| Customer Need | Traditional Approach | AI-Integrated Approach |

| Loan application | 5-10 days, multiple document submissions | Instant decision with one-click document upload |

| Fraud alert | Discover fraudulent charges on statement | Real-time alert before transaction completes |

| Financial advice | Generic tips or expensive advisor meetings | Personalized recommendations based on spending patterns |

| Problem resolution | 15-minute wait, transferred between departments | Chatbot resolves 70% of issues instantly with full context |

| Product discovery | Mass marketing hoping something sticks | Proactive suggestions timed to life events |

Delivering this kind of experience requires AI that’s deeply integrated into customer-facing systems. When someone opens the banking app, the personalization engine needs to pull their transaction history, assess their current financial position, and determine what information or offers might be relevant, all in milliseconds.

This level of integration is technically challenging because it involves real-time data access, rapid decision making, and smooth handoffs between automated and human channels. The financial institutions getting this right are seeing measurable improvements in customer satisfaction, product adoption, and retention. Those that haven’t invested in proper integration are still offering generic experiences that increasingly feel outdated.

How AI Integration Improves the Financial Technology Stack

Core Banking Modernization

Core banking systems are the foundational platforms that handle accounts, transactions, and customer records. Many of these systems were built decades ago and were never designed to support AI. They use outdated data formats, lack modern APIs, and run on infrastructure that can’t handle the computational demands of machine learning.

Completely replacing core banking systems is enormously expensive and risky. Most institutions choose instead to modernize incrementally by adding AI-enabled components that enhance specific functions.

The Modernization Path:

Phase 1 – API Wrapping: Create modern APIs around legacy systems so AI services can access core data without direct system modification. This provides the foundation for everything else.

Phase 2 – Microservices Layer: Build new AI-powered services that handle specific intelligent functions (fraud detection, personalization, credit decisioning) while still using the core system for record keeping.

Phase 3 – Event-Driven Architecture: Implement real-time data streaming so AI models can respond to events as they happen rather than working from batch updates.

Phase 4 – Gradual Core Replacement: Over time, shift critical functions from legacy systems to modern platforms, but only after proving the new approach works reliably at scale.

The integration challenge involves making old and new components work together reliably while maintaining the performance and security that banking operations require. Done well, this approach lets institutions gain AI capabilities without the massive risk and cost of replacing everything at once.

AI-enabled Risk and Fraud Management

Fraud detection represents one of the most mature applications of AI in finance, but effectiveness depends heavily on integration quality. According to research published in the Journal of Financial Crime, AI-based fraud detection systems can identify up to 95% of fraudulent transactions while reducing false positives by 70% compared to rule-based systems.

How Modern Fraud Detection Works

A fraud detection model needs access to multiple data sources simultaneously:

- Transaction details (amount, merchant, location, time)

- Customer historical patterns (typical spending, locations, merchants)

- Device fingerprints (is this their usual phone or computer?)

- Behavioral biometrics (typing patterns, navigation behavior)

- Network analysis (connections to known fraud patterns)

- External threat intelligence (compromised merchant data, fraud trends)

The system analyzes hundreds of variables per transaction in milliseconds, looking for subtle anomalies that rule-based systems would miss. These might include unusual transaction timing, geographic inconsistencies, or behavioral patterns that deviate from established norms.

What Proper Integration Enables:

The difference between a good model and an effective system comes down to integration. When the model identifies suspicious activity, the integration layer determines what happens next. Low-risk anomalies might generate a notification asking the customer to confirm the transaction. Medium-risk patterns could trigger step-up authentication before proceeding. High-risk transactions get blocked immediately and routed to investigators with all relevant context already assembled.

The models continuously learn from new fraud patterns, adapting without requiring manual reprogramming. But none of this works unless the integration layer can deliver data quickly enough, handle the computational load, and route decisions to the right systems for action.

Risk management extends beyond fraud to include credit risk, market risk, and operational risk. AI models that assess these risks need integration with data warehouses, trading systems, loan portfolios, and external market data feeds. The outputs need to flow into risk dashboards, capital allocation systems, and regulatory reporting platforms.

Real-time Decisioning Engines

Speed matters in modern finance. Customers expect instant responses when they apply for credit cards or request loan approvals. Traders need split-second decisions on whether to execute transactions. Payment processors must approve or decline transactions in milliseconds to avoid frustrating customers at checkout.

| Decision Type | Traditional Timeline | AI-Integrated Timeline | Accuracy Improvement |

| Credit card approval | 7-10 days | Under 60 seconds | +15% default prediction |

| Personal loan | 3-5 days | 2-10 minutes | +22% risk assessment |

| Mortgage pre-approval | 2-3 weeks | Same day | +18% applicant quality |

| Transaction approval | 2-3 seconds | Under 500ms | +40% fraud detection |

Traditional decisioning processes involved sequential steps with multiple handoffs and waiting periods. An application would move through credit checks, fraud screening, income verification, and final approval over days or weeks. AI-powered decisioning engines can complete all these steps in seconds by running multiple assessments in parallel and synthesizing the results into a final decision.

This requires integration that connects to credit bureaus, internal customer data, fraud detection systems, and policy engines, all while maintaining audit trails that document the decision logic. The technical challenge involves not just speed but reliability. A decisioning engine that’s wrong 5% of the time but fast is worse than a slower system that’s more accurate.

The accuracy improvements are as important as the speed gains. AI models can incorporate more variables and detect more subtle patterns than traditional scoring methods. They can assess risk more precisely by considering factors that humans might miss or weigh incorrectly.

Intelligent Automation in Operations

Back-office operations in financial institutions involve enormous amounts of document processing, data entry, exception handling, and verification work. Much of this has traditionally required human review because the documents and data are unstructured or semi-structured, making them difficult for traditional software to handle.

What AI Can Now Automate:

Document Processing: AI systems can read loan applications, extract relevant information, verify it against other sources, and route exceptions for human review. They process identity documents for KYC checks, flagging potential issues while automatically approving clear cases.

Dispute Resolution: Analyze customer disputes, determine likely outcomes based on similar historical cases, and suggest resolution approaches. For straightforward disputes, handle resolution automatically.

Contract Analysis: Review contracts, identify key terms, and alert to non-standard provisions. Extract critical dates, obligations, and conditions into structured data that other systems can use.

Customer Communication: Natural language processing can analyze emails, chat messages, and support tickets to determine intent, extract key information, and either respond automatically or route to the appropriate specialist with context included.

The value comes from integration that embeds these capabilities into existing workflows. Document processing AI needs to connect to document management systems, customer databases, and case management platforms. The automation needs to handle straight-through processing for routine cases while seamlessly escalating exceptions to human workers with all necessary context included.

According to MIT Sloan research on AI in operations, organizations that successfully integrate AI into operational workflows see productivity improvements of 30-40% in affected areas, with the benefits accumulating as the AI learns from more examples over time.

Business Outcomes of AI Integration

Cost Reduction and Efficiency Gains

The most immediate impact of successful AI integration shows up in operational costs. The numbers are significant:

Documented Cost Impacts:

- Transaction processing: 40-60% reduction in cost per transaction

- Customer service: 30-50% reduction in agent-handled interactions

- Document processing: 70-80% reduction in processing time

- Compliance review: 50-65% reduction in manual review hours

- Back-office operations: 25-40% reduction in operational headcount needs

But the efficiency gains extend beyond simple cost cutting. Staff who previously spent their time on routine tasks can focus on work that requires human judgment and expertise. Processing times decrease, which improves customer satisfaction and enables higher transaction volumes without proportional increases in headcount. Error rates drop because AI systems apply rules consistently rather than making the occasional mistakes that humans inevitably make with repetitive work.

Consider a mid-sized bank processing 50,000 transactions daily. If manual review costs $3 per transaction and AI integration reduces the need for manual review by 70%, that’s $105,000 in daily savings or roughly $38 million annually. Even after accounting for the cost of the AI systems themselves, the ROI becomes compelling quickly.

The returns compound over time as organizations expand AI integration to additional processes and as the models themselves improve through continued learning. Financial institutions that implemented comprehensive AI integration three to five years ago are now seeing benefits that exceed their initial projections because the technology has continued improving.

Enhanced Security and Risk Mitigation

Security incidents are expensive in financial services, both in direct costs and reputational damage. A single data breach or fraud event can cost millions in losses, regulatory fines, and customer remediation.

The Security Impact of AI Integration

Prevention: Behavioral analytics identify compromised accounts by noticing subtle changes in usage patterns before significant damage occurs. Anomaly detection spots unusual system access that might indicate insider threats. Network monitoring identifies suspicious traffic patterns that could signal cyberattacks.

Detection: Transaction monitoring catches fraud attempts faster, often before losses occur. Pattern recognition identifies coordinated fraud rings that individual transaction reviews would miss. Real-time analysis spots emerging attack patterns that haven’t been seen before.

Response: Automated incident response can contain threats immediately rather than waiting for human analysts to notice and react. Integration with security systems enables coordinated responses across multiple platforms simultaneously.

A study from Juniper Research found that AI-based fraud detection will prevent $11 billion in losses annually by 2025, up from $6 billion in 2021. The institutions seeing the best results are those that have integrated AI across their entire risk management framework rather than deploying it in isolated pockets.

Risk mitigation extends to credit risk, where better scoring models reduce default rates, and operational risk, where AI can predict equipment failures or process bottlenecks before they cause problems. The cumulative effect of small improvements across many risk areas adds up to significant overall risk reduction.

Revenue Growth and New Business Models

While cost reduction gets attention, revenue impact can be even more significant. Here’s where AI integration drives top-line growth:

| Revenue Driver | Mechanism | Typical Impact |

| Product adoption | AI-enabled personalization recommends relevant offerings | 15-25% increase in cross-sell |

| Customer expansion | Better credit models profitably serve new segments | 10-15% market expansion |

| Transaction volume | Faster processing enables higher throughput | 20-30% capacity increase |

| Premium services | AI-powered features justify higher fees | 5-10% revenue per customer |

| Retention | Better experience reduces churn | 8-12% churn reduction |

Some institutions are using AI integration to enable entirely new business models:

Real-time Payments Infrastructure: AI decisioning enables instant payments with fraud protection that works at scale. This opens markets in peer-to-peer transfers, instant merchant settlements, and cross-border transactions that traditional systems couldn’t handle profitably.

Embedded Finance: Putting banking services inside non-financial apps (like buy-now-pay-later at checkout) requires AI that can make credit decisions in milliseconds while the customer is actively shopping.

Usage-based Products: Insurance products that adjust pricing based on actual behavior rather than demographic proxies. Investment products that automatically rebalance based on market conditions and individual goals.

Hyper-personalization: Moving beyond segment-based marketing to individual-level product design, pricing, and recommendations.

These innovations only work with sophisticated AI integration that can handle the speed, scale, and complexity they require. The competitive dynamics are shifting toward institutions that can use AI to serve customers better, move faster, and operate more efficiently. The revenue impact comes not just from individual AI applications but from the cumulative advantage of operating as a more intelligent organization.

Challenges Facing Financial Institutions in AI Integration

Data Fragmentation and Data Governance

Financial institutions typically have data scattered across dozens or hundreds of systems, each with its own schema, quality standards, and access controls. This isn’t just inconvenient, it’s a fundamental barrier to AI success.

The Typical Data Landscape:

- Customer information exists in the core banking system, CRM platform, marketing automation tools, and various product-specific databases

- Transaction data flows through payment processors, card networks, and settlement systems

- Risk data comes from internal models, credit bureaus, and external data providers

- Historical records might exist in archived systems that are no longer actively maintained

- Document storage spans multiple platforms with inconsistent metadata

Getting this data into a form that AI models can use requires significant data engineering work. It means building pipelines that extract data from source systems, transform it into consistent formats, handle missing or inconsistent values, and load it into platforms where models can access it.

Then there’s governance. Who owns each data element? What quality standards apply? Who can access what information? How long should data be retained? What happens when data protection regulations conflict with record-keeping requirements?

Common Data Quality Issues That Break AI:

- Customer records with different addresses across systems (which is current?)

- Transaction amounts in different currencies without proper conversion tracking

- Dates in incompatible formats (MM/DD/YYYY vs DD/MM/YYYY causes real problems)

- Missing values that mean different things (null, zero, not applicable, unknown)

- Duplicate records with slightly different identifying information

- Historical data that uses obsolete codes or categories

Many AI integration projects fail not because of problems with the models but because the underlying data infrastructure was inadequate. A model trained on clean, complete data will produce garbage results when deployed against real-world data that’s messy and inconsistent.

Addressing this requires investment in data engineering capabilities and often some difficult organizational work to establish governance structures that span traditional silos. The institutions that get this right treat data infrastructure as a strategic asset rather than just an IT concern.

Integration With Legacy Infrastructure

Legacy systems present both technical and organizational challenges. The technical problems are significant:

Technical Barriers:

- Systems built in programming languages (COBOL, Fortran) where skilled developers are scarce and expensive

- Mainframes that can’t easily scale to handle AI computational loads

- Batch processing architectures that conflict with real-time AI requirements

- Missing documentation for critical systems (the people who built them retired years ago)

- Hard-coded business rules scattered throughout the codebase

- Database structures optimized for 1980s hardware constraints

Making AI work with these systems sometimes requires building elaborate middleware layers that translate between old and new technologies. An AI model might produce outputs in JSON format that need conversion to fixed-width text files for the mainframe. Real-time API calls might need to wait for nightly batch processes to complete. Modern authentication might need to work with systems that expect different security models.

Organizational Challenges:

- IT teams responsible for legacy systems resist changes that might create risk

- Budget allocation favors keeping existing systems running over modernization

- Business units depend on legacy system behavior and worry about disruption

- Compliance teams need extensive validation that new approaches meet regulatory requirements

- Limited expertise means few people understand both legacy systems and modern AI

These concerns aren’t irrational. A core banking system that processes millions of transactions daily can’t have an outage, even briefly. When the system has run reliably for 20 years, any change introduces risk. The people responsible for maintaining uptime naturally approach integration cautiously.

Successful AI integration in these environments requires patience, careful planning, and usually a phased approach that proves each step works reliably before moving to the next. Quick wins matter because they build confidence and demonstrate value, making it easier to secure support for more ambitious integration work.

Explainability and Model Risk

Financial services is a regulated industry where decisions often need explanation. When a model denies someone credit or flags a transaction as fraudulent, the institution may need to explain why. Some regulations explicitly require that automated decisions be explainable to consumers.

This creates tension with some AI approaches. Deep learning models can be remarkably accurate but notoriously difficult to explain. They learn complex patterns from data, but extracting simple explanations of why they made specific decisions isn’t always possible. A neural network might correctly identify fraudulent transactions 95% of the time but only tell you it did so based on “patterns in the data” without specifics.

The Explainability Spectrum:

| Model Type | Accuracy | Explainability | Common Use |

| Simple rules | Low | Perfect | Regulatory compliance baselines |

| Decision trees | Medium | Good | Credit decisions requiring explanation |

| Ensemble methods | High | Moderate | Risk assessment with feature importance |

| Neural networks | Very high | Poor | Fraud detection where accuracy matters most |

Model risk extends beyond explainability. Models can fail in subtle ways:

- They might work well on training data but degrade in production as conditions change

- They can perpetuate or amplify biases present in historical data

- They may perform poorly on edge cases that rarely occurred in training

- They can become overconfident, providing precise but inaccurate predictions

Financial institutions need robust model risk management frameworks that include regular performance monitoring, bias testing, sensitivity analysis, and validation against independent datasets. The integration work needs to include monitoring infrastructure that tracks model behavior and alerts when performance degrades.

Regulators are paying increasing attention to AI risk management. The Basel Committee on Banking Supervision has published guidance on managing risks from third-party AI vendors, while various national regulators have issued their own requirements. Integration projects need to address these concerns from the start rather than treating them as afterthoughts.

Talent Gap and Vendor Dependence

The skills required for successful AI integration span multiple domains: data engineering, machine learning, software architecture, financial services knowledge, regulatory compliance, and change management. Finding people who combine these skills is difficult and expensive.

The Talent Challenge:

Data Scientists understand machine learning but may lack experience with production systems and financial services regulations. They can build great models that don’t work well in real banking environments.

Software Engineers understand building reliable systems but may not grasp machine learning subtleties. They might deploy models incorrectly or fail to implement proper monitoring.

Domain Experts understand banking operations and regulations but may lack technical depth. They know what needs to happen but not how to make it happen technically.

Integration Specialists who understand all three areas are rare and command premium compensation.

This talent gap drives many institutions toward vendor relationships. Working with specialized AI integration partners provides access to expertise without building entire teams internally. But vendor dependence creates its own risks:

- Loss of control over critical capabilities

- Difficulty switching vendors if the relationship sours

- Knowledge remaining with the vendor rather than building internal capability

- Potential conflicts of interest if the vendor works with competitors

- Dependency on vendor roadmaps and priorities

The most successful approaches balance external expertise with internal capability development. Bring in partners for specialized work while ensuring internal teams learn enough to effectively manage the relationship and make informed decisions. Over time, shift more capabilities in-house as the organization builds expertise.

Some institutions create centers of excellence that combine internal and external talent, building hybrid teams that can tackle integration challenges while gradually reducing vendor dependence. This approach works but requires executive commitment and patient investment in capability building.

Best Practices for Successful AI Integration

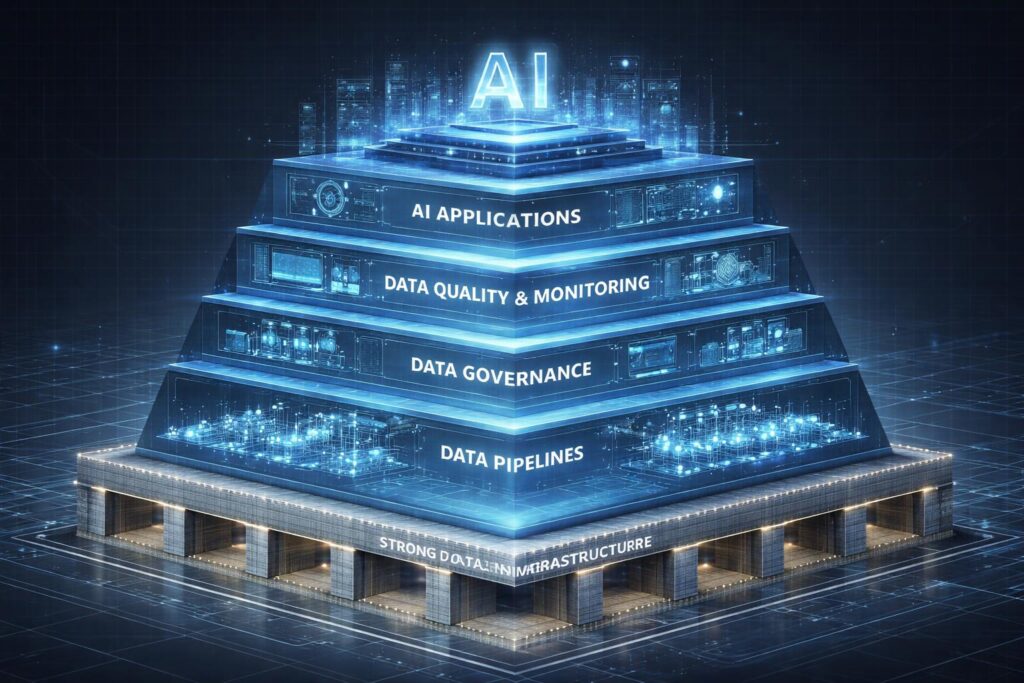

Building a Unified Data Foundation

AI is only as good as the data it learns from. Everything else depends on getting this right first.

Essential Data Infrastructure Components:

Data Lakes and Warehouses: Central repositories where data from across the organization can be stored in formats suitable for AI. Data lakes handle raw, unstructured data while warehouses store cleaned, structured data ready for analysis.

Data Pipelines: Automated processes that extract data from source systems, transform it into consistent formats, validate quality, and load it into central repositories. These need to run reliably, handle errors gracefully, and provide monitoring visibility.

Data Catalog: Documentation of what data exists, where it comes from, what it means, and who’s responsible for it. Seems basic but many organizations lack this, leading to endless confusion about which dataset to trust.

Quality Monitoring: Automated checks that catch data quality problems before they reach AI models. This includes completeness checks, format validation, range verification, and consistency testing across related data elements.

Access Controls: Security infrastructure that ensures data gets used appropriately while remaining accessible to legitimate users. This includes encryption, authentication, authorization, and audit logging.

The institutions that excel at AI integration typically spent years building data infrastructure before their AI efforts really took off. They treated data as a strategic asset and made the investments required to manage it properly. Those that tried to shortcut this step found their AI projects repeatedly stalling due to data problems.

Adopting an Incremental AI Roadmap

Trying to transform everything at once is a recipe for failure. Successful AI integration follows a deliberate progression:

Phase 1 – Pilot Projects: Start with well-defined use cases that have clear success metrics and limited scope. Fraud detection for a single product line. Chatbot handling one category of customer inquiries. Credit decisioning for a specific customer segment. The goal is proving the approach works and building organizational confidence.

Phase 2 – Expand Successful Pilots: Take what worked in pilots and expand to broader scope. If fraud detection worked for credit cards, expand to other transaction types. If the chatbot handled account inquiries well, add more capabilities. This phase focuses on scaling proven approaches.

Phase 3 – Platform Development: Build reusable infrastructure that makes future AI integration easier. Standard data pipelines, shared model deployment platforms, common monitoring tools. This investment pays off as you tackle more use cases.

Phase 4 – Enterprise Maturity: AI becomes embedded across operations with governance frameworks, established processes, internal expertise, and continuous improvement. New AI capabilities can be added quickly because the infrastructure and knowledge exist.

This progression typically takes three to five years. Organizations that try to jump directly to enterprise maturity usually struggle because they lack the learning from earlier phases. Each phase builds capabilities needed for the next.

Critical Success Factors at Each Phase:

- Pilot: Clear metrics, executive sponsorship, cross-functional teams, permission to fail

- Expansion: Standardized approaches, knowledge transfer, resource scaling

- Platform: Architectural vision, significant investment, technical leadership

- Maturity: Cultural adoption, continuous learning, innovation pipeline

Ensuring Compliance and Model Governance

AI governance isn’t optional in financial services. Regulators expect institutions to understand how their AI systems work, validate that they operate correctly, and demonstrate they’re being used appropriately.

Core Governance Requirements:

Model Documentation: Clear descriptions of what each model does, how it was developed, what data it uses, what assumptions it makes, and what limitations it has. This needs to be understandable by non-technical stakeholders and regulators.

Validation Process: Independent testing that confirms models work as intended, perform accurately on new data, and don’t have unintended biases or failure modes. Validation should happen before deployment and periodically thereafter.

Performance Monitoring: Continuous tracking of model accuracy, stability, and business impact. Systems should alert when performance degrades or unexpected patterns emerge.

Change Management: Formal processes for updating models, with testing and approval before changes reach production. Documentation of what changed, why, and what impact it had.

Bias Testing: Regular assessment of whether models treat different customer groups fairly. This includes testing for disparate impact and examining whether decisions would be considered discriminatory.

Audit Trails: Complete records of model decisions, inputs that drove those decisions, and any human overrides. This enables investigation when problems occur and demonstrates compliance to regulators.

Building this governance infrastructure requires investment but pays off in risk reduction and regulatory confidence. Institutions with strong governance can deploy AI more quickly because they have systematic ways to validate safety and compliance.

Choosing the Right AI Integration Partner

Most financial institutions will work with external partners for at least some AI integration work. Choosing the right partner makes an enormous difference in outcomes.

Essential Partner Capabilities:

Financial Services Domain Expertise: Understanding banking operations, regulatory requirements, and industry-specific challenges. Partners without this background will make costly mistakes.

Large-scale Integration Experience: Proven track record deploying AI in complex enterprise environments with legacy systems. Small pilot projects are very different from production deployments at scale.

MLOps Competency: Expertise in the operational aspects of running AI systems, including model deployment, monitoring, updating, and governance. Many partners can build models but lack MLOps depth.

Technology Stack Breadth: Experience with the various technologies financial institutions use, from modern cloud platforms to legacy mainframes. The ability to work across this range is essential.

Security and Compliance Focus: Understanding of financial services security requirements and regulatory frameworks. The partner should view these as design constraints, not afterthoughts.

Warning Signs of Poor Partners:

- Over-promising capabilities or timelines that seem unrealistic

- Limited references from similar organizations or use cases

- Focusing primarily on model accuracy without addressing integration challenges

- Proposing purely cloud-based solutions without understanding on-premise requirements

- Lack of clarity about ongoing support and maintenance

- Insufficient attention to documentation and knowledge transfer

The best partnerships combine external expertise with internal capability building. The partner should be teaching your team, not just doing work for them. Over time, you want to reduce dependence even on good partners by building internal competence.

Real-world Case Illustrations

Case 1: European Bank Modernizes Credit Decisioning

A major European retail bank was struggling with credit application processing that took 5-7 days on average and required significant manual review. Their legacy credit scoring system used relatively few variables and couldn’t incorporate newer data sources like transaction patterns or digital behavior. This led to two problems: good customers were being rejected based on traditional metrics, and bad loans were being approved because the scoring missed warning signs.

The Integration Challenge: The bank’s core systems were built on a mainframe architecture from the 1990s. Credit decisions involved multiple systems that didn’t communicate well with each other. Customer data existed in fragmented form across dozens of databases. The existing process had evolved over decades and was deeply embedded in operational workflows.

Integration Approach: Rather than replacing everything, the bank implemented a layer of AI services that sat between customer-facing applications and core systems. They built data pipelines that pulled information from various sources in near real-time, creating unified customer profiles that AI models could analyze. The credit decisioning model itself incorporated over 200 variables including transaction history, digital engagement patterns, and behavioral signals. The integration layer handled translation between modern APIs and legacy systems, managed workflow routing, and provided the monitoring infrastructure.

Results: Credit decisions that previously took days now complete in under 90 seconds for 85% of applications. Default rates decreased by 18% because the models identify risk more accurately. Customer satisfaction improved significantly due to faster decisions. The bank estimates they’re serving 15% more customers profitably than they could with the old system. Perhaps most importantly, the integration approach proved that they could modernize incrementally without massive disruption, building confidence for additional AI initiatives.

Case 2: Asian Insurance Company Automates Claims Processing

A large Asian insurance provider processed over 2 million claims annually, with 60% requiring manual document review and data entry. The average claim took 7-10 days to process, creating customer frustration and operational bottlenecks. During peak periods like natural disasters, the backlog would grow to weeks. The company employed over 800 people primarily for manual claims processing.

The Integration Challenge: Claims arrived through multiple channels including paper mail, email, mobile apps, and agent portals. Each had different formats and quality levels. The documents were semi-structured at best: medical bills, receipts, accident reports, and supporting materials that AI needed to understand. These needed to connect to policy systems, payment processors, and fraud detection while maintaining complete audit trails for regulatory compliance.

Integration Approach: The company implemented computer vision models for document classification and optical character recognition, natural language processing for extracting key information from unstructured text, and machine learning models for fraud detection and claim validation. The integration layer managed document routing, orchestrated multiple AI models working in sequence, handled exceptions that needed human review, and maintained connections to existing policy and payment systems. Critically, the integration included a feedback loop where human reviewers could correct AI mistakes, improving the models over time.

Results: 75% of claims now process completely automatically without human review. Processing time dropped from 7-10 days to under 2 hours for automated claims. The operational staff shifted from data entry to handling complex cases and customer service. Fraud detection improved, with the AI identifying suspicious patterns that manual review missed. The company estimates annual savings of $45 million while simultaneously improving customer satisfaction scores by 28 points.

Case 3: North American Payment Processor Enhances Fraud Detection

A payment processor handling billions in monthly transaction volume faced increasing fraud losses despite having a fraud detection system. Traditional rule-based approaches couldn’t keep pace with evolving fraud patterns. False positive rates were high, declining legitimate transactions and frustrating customers. The fraud team spent most of their time investigating false alarms rather than actual fraud.

The Integration Challenge: The payment system processed transactions in real-time with latency requirements under 100 milliseconds. The AI needed to analyze each transaction against historical patterns, device fingerprints, merchant risk profiles, and network analysis, all while meeting strict performance requirements. The integration had to work across multiple data centers with no single point of failure. Changes needed to deploy without disrupting live transaction processing.

Integration Approach: The company built a distributed AI infrastructure that could analyze transactions in parallel across multiple servers. The integration layer pulled data from transaction streams, customer databases, device intelligence systems, and external threat feeds, creating a comprehensive view for each transaction in real-time. The AI models ran in production alongside the existing rule-based system, initially in shadow mode to prove reliability. The integration included sophisticated fallback mechanisms: if AI components failed, transactions would fall back to rule-based processing without customer impact.

Results: Fraud detection accuracy improved from 76% to 94%, meaning the system correctly identifies nearly all fraud attempts. False positive rates dropped by 68%, resulting in far fewer legitimate transactions being declined. The improvements translate to $180 million in prevented fraud losses annually while reducing customer friction. Perhaps more impressively, the system now detects new fraud patterns within hours of their emergence rather than weeks, as the AI continuously learns from incoming data. The fraud investigation team focuses on sophisticated attacks rather than reviewing obvious false positives.

Case 4: Global Bank Transforms Customer Service

A multinational bank with 15 million customers handled over 50,000 customer service contacts daily across phone, chat, and email. Customer wait times averaged 12-15 minutes during peak hours. The bank employed 3,000 customer service representatives, yet satisfaction scores remained mediocre. Many customer inquiries were routine questions that didn’t require specialized expertise but still consumed significant representative time.

The Integration Challenge: Customer service systems needed access to account information, transaction history, product details, and prior interactions. The AI chatbot needed to understand customer intent from natural language, retrieve relevant information from multiple systems, determine appropriate responses, and escalate complex issues to human representatives smoothly with full context. Different customer segments required different service approaches. Regulatory requirements mandated specific disclosures for certain types of interactions.

Integration Approach: The bank deployed conversational AI with deep integration into their customer service ecosystem. Natural language understanding determined customer intent and extracted key information from requests. The integration layer connected to CRM systems, account databases, transaction processors, and product catalogs to retrieve necessary information. The system included intelligent routing that assessed inquiry complexity and customer value to determine automated versus human handling. When escalation occurred, representatives received complete conversation history and relevant account information automatically. The integration maintained compliance by automatically including required disclosures and creating proper documentation.

Results: The AI now handles 68% of customer inquiries completely without human intervention. Average wait times for human representatives dropped to under 3 minutes because they only handle complex issues. Customer satisfaction scores improved by 34 points. The bank redeployed customer service staff to relationship management and sales roles where human expertise adds more value. Cost per interaction decreased by 58%. Most surprisingly, many customers now prefer the AI interaction because it’s faster and available 24/7, with satisfaction scores for automated interactions exceeding those for human interactions in certain inquiry categories.

Conclusion

The wave of investment in AI integration services by financial institutions reflects a fundamental shift in how these organizations view technology. AI has moved from experimental technology to strategic necessity. The institutions making substantial investments today recognize that competitive advantage increasingly depends on the ability to make better decisions faster, serve customers more effectively, manage risk more precisely, and operate more efficiently than competitors.

What separates successful AI adoption from failed experiments is almost always integration quality rather than model sophistication. The financial services graveyard is full of impressive AI models that never made it to production because nobody figured out how to connect them to existing systems, maintain them reliably, or operate them at the scale and security standards that banking requires. The institutions seeing real business impact from AI have made integration a strategic priority, investing in the data infrastructure, technical capabilities, governance frameworks, and organizational changes required to embed intelligence throughout their operations.

Looking forward, the gap between AI leaders and laggards in financial services will likely widen. The institutions that have built strong integration capabilities can add new AI applications quickly, while those still struggling with basics will find themselves perpetually behind. The compounding effects of better customer experience, more efficient operations, and superior risk management create advantages that become increasingly difficult to overcome. According to industry analysts, spending on AI integration services in financial services is projected to grow at over 25% annually through 2028, driven by institutions that have seen results and are expanding their efforts, as well as laggards finally recognizing they must move or accept diminishing relevance.

For financial services leaders evaluating their AI strategy, the question is no longer whether to invest in integration but how quickly they can build the capabilities required to compete effectively. The institutions that will thrive in the next decade are those treating AI integration as a core competency rather than an IT project, making the necessary investments in data infrastructure and talent, and approaching the work with appropriate ambition tempered by realistic timelines and rigorous governance.

Partner With Experts in Financial AI Integration

The journey from AI experiments to production-grade systems that deliver measurable business value requires specialized expertise spanning machine learning, financial services operations, regulatory compliance, and enterprise integration. Organizations that try to build all this capability internally often underestimate the complexity and timeline required, while those that choose the wrong partners find themselves with systems that don’t actually work in production environments.

Our team brings deep experience in financial AI integration, with proven results deploying intelligent systems at scale for banks, insurance companies, and payment processors. We understand the unique challenges of integrating AI with legacy infrastructure, maintaining security and compliance standards, and building systems that operate reliably under production conditions. More importantly, we focus on transferring knowledge to your team rather than creating dependency, ensuring you build internal capability while leveraging our expertise.

If you’re exploring how AI integration can transform your operations, we invite you to schedule a consultation. We’ll discuss your specific challenges, evaluate your current technology landscape, and outline a realistic roadmap for achieving your goals. Whether you’re just beginning your AI journey or looking to scale initial successes across the enterprise, we can help you navigate the complexity and deliver real business outcomes.

Learn more about our AI integration services, explore our fintech software development capabilities, or review detailed case studies from similar institutions. For organizations building the data foundation required for AI success, our data engineering and MLOps practices provide the infrastructure and operational excellence that make the difference between experiments and production systems.