Every payment transaction your platform processes is a potential point of failure, a compliance event, and a trust signal — all at the same time. Engineers who treat gateway integration as a weekend task discover this the hard way, usually at 2 AM after a double-charge incident surfaces in production with real customer money on the line.

This guide won’t give you a surface-level walkthrough of API keys and curl commands. What follows is a complete architectural blueprint for payment gateway integration — covering service isolation, idempotency design, webhook hardening, PCI DSS scope reduction, and transactional integrity at the database layer. By the end, you’ll have the engineering foundation to build payment infrastructure that survives network partitions, regulatory audits, and scale.

We’ll benchmark Stripe, Adyen, and Braintree against the decisions that actually matter architecturally. We’ll work through idempotency key implementation with Redis locks. We’ll design a normalized SQL ledger schema that holds up under concurrent writes. And we’ll cover the testing matrix you need before a single real card is charged.

Why Payment Infrastructure Demands Architectural Discipline

FinTech startups operating in 2025 face a harder problem than most engineering teams acknowledge. You’re not just integrating an API — you’re building a distributed system where network failures are probabilistic, third-party gateway SLAs are never 100%, and regulatory frameworks like PCI DSS dictate what your infrastructure is even allowed to look like.

The blast radius of a poorly designed payment integration is asymmetric. A bug in your product catalog is embarrassing. A double-charge bug is a chargeback, a support escalation, and a trust erosion event that compounds. The engineering discipline required here is closer to financial systems design than web development, and your architecture should reflect that.

Genius Software’s FinTech software development practice has consistently found that teams underinvest in three areas: idempotency, webhook reliability, and database transaction design. These are exactly what this guide focuses on.

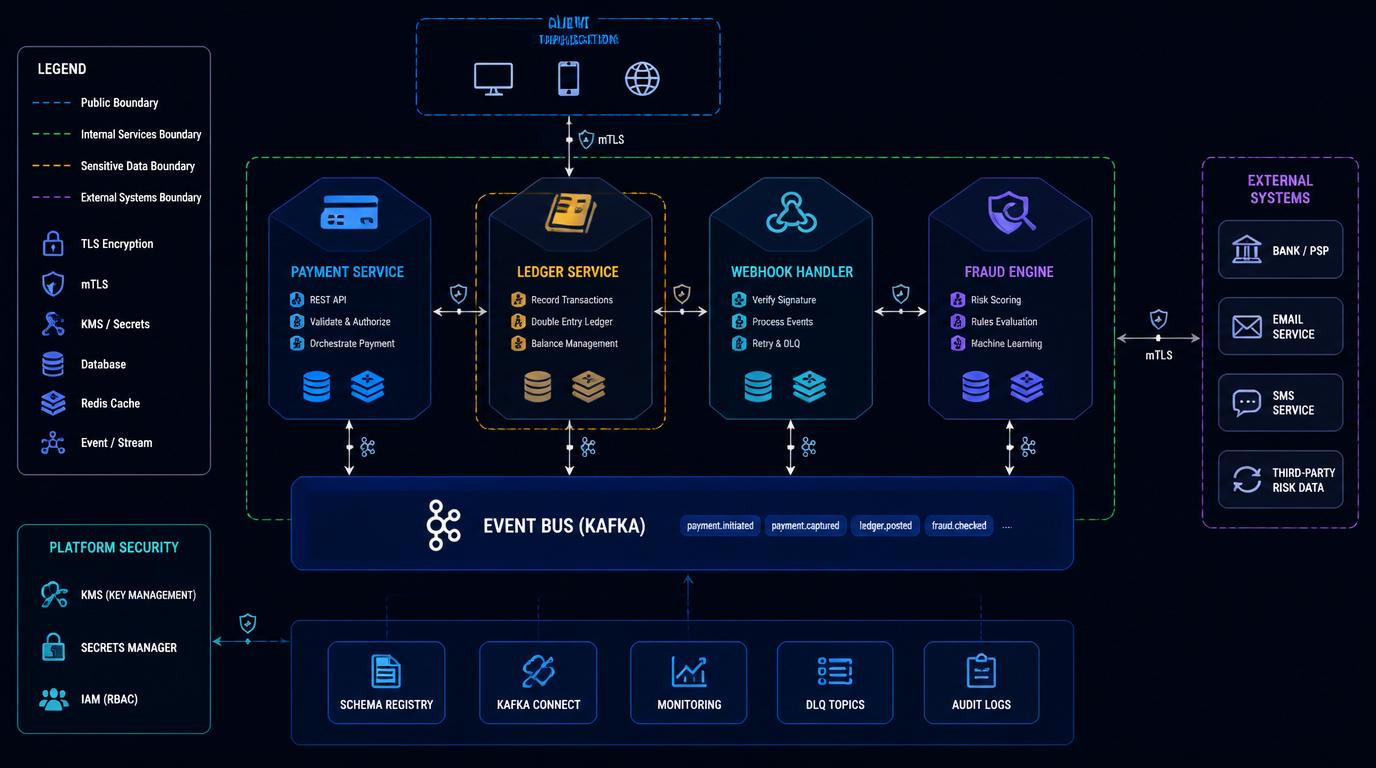

Architectural Blueprint: Monolith vs. Microservices for Payments

The Case for Service Isolation

Running payment logic inside a monolithic application creates four compounding risks: shared failure domains, PCI DSS scope expansion, scaling entanglement, and deployment coupling. When your payments code lives inside the same process as your user management and product catalog, a memory leak in the product service can cascade into payment latency. Worse, PCI DSS Level 1 compliance requires you to demonstrate control over cardholder data environments — which is nearly impossible to scope narrowly when everything shares a runtime.

The correct architecture isolates payment concerns behind a dedicated Payment Service with its own database, its own deployment pipeline, and its own network perimeter. This isn’t premature optimization; it’s the minimum viable security boundary for handling card data in production.

A well-designed payment microservices topology includes these bounded contexts:

- Payment Service — Orchestrates charge initiation, handles idempotency enforcement, and coordinates with the gateway API. Owns no card data directly.

- Ledger Service — Maintains the authoritative double-entry accounting record of all financial movements. Append-only writes, read replicas for reporting.

- Webhook Processor — Receives, verifies, deduplicates, and dispatches gateway callbacks. Decoupled from the Payment Service via an internal event bus.

- Fraud & Risk Engine — Pre-authorization scoring using behavioral signals, IP reputation, and velocity checks. Plugged in as a synchronous gate before charge initiation.

- Notification Service — Consumes downstream payment events and triggers user-facing communications.

Event-driven communication between these services — via Apache Kafka or AWS SNS/SQS depending on your infrastructure preferences — provides the loose coupling that lets each service scale, deploy, and fail independently.

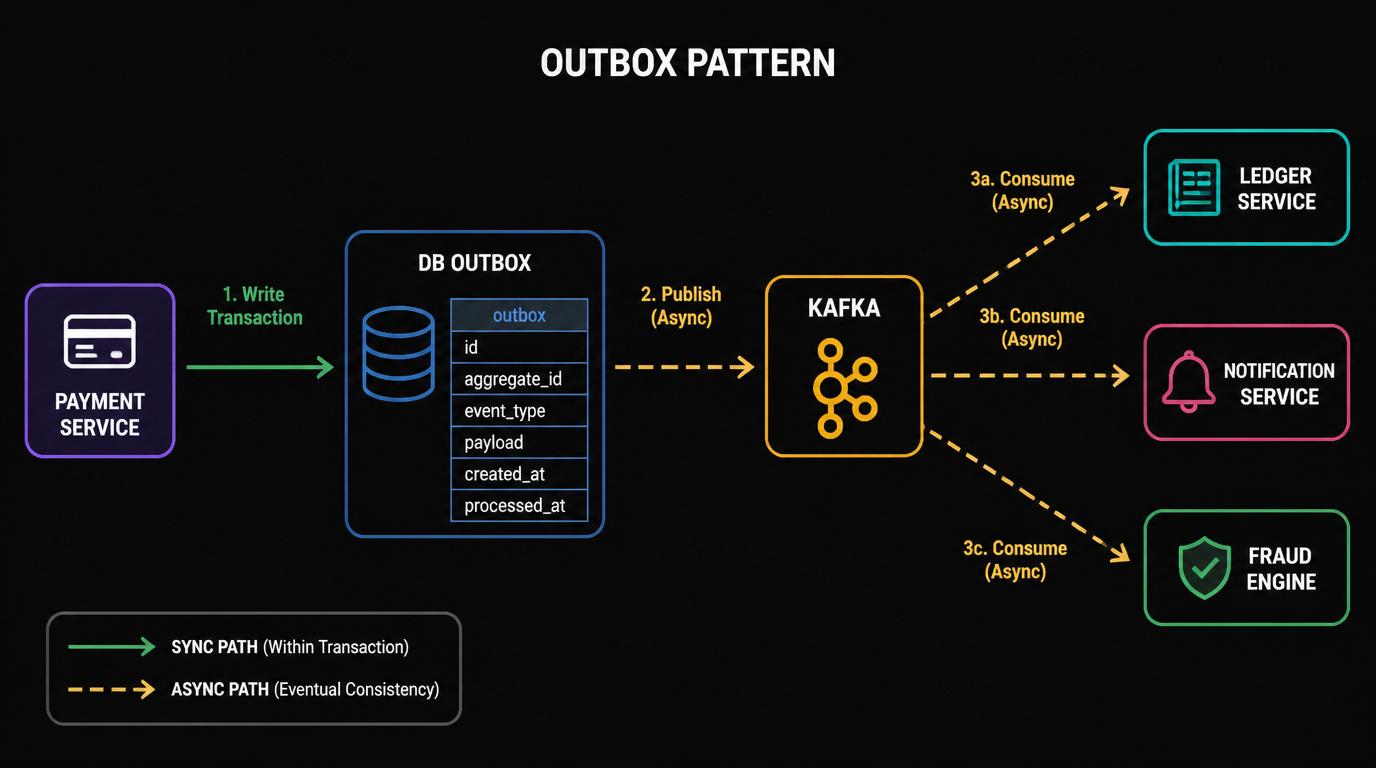

Event-Driven Patterns for Transaction Processing

Synchronous, request-response payment flows are fragile. If your Payment Service calls your Ledger Service synchronously and the ledger is under load, you’ve introduced a dependency that degrades your checkout conversion rate. The more resilient pattern uses an outbox pattern at the database level: the Payment Service writes the transaction record and an outbox event atomically in the same database transaction, then a separate relay process publishes that event to Kafka. Downstream consumers (Ledger, Notifications) process it asynchronously.

This gives you durability guarantees that a direct service-to-service HTTP call simply cannot provide.

Payment Gateway Benchmark: Stripe vs. Adyen vs. Braintree

Choosing a gateway is an architectural decision that compounds over time. The wrong choice at Series A becomes a multi-quarter migration project at Series B. Evaluate against your actual engineering constraints, not marketing pages.

| Dimension | Stripe | Adyen | Braintree (PayPal) |

|---|---|---|---|

| API Design Quality | REST + strongly typed SDKs; excellent developer ergonomics; versioned endpoints | REST with JSON; robust but more enterprise-verbose; better for complex flows | REST; solid but less modern; PayPal ecosystem coupling is a friction point |

| Global Payout Routing | Stripe Connect handles marketplace payouts; strong in US/EU/AU | Best-in-class global acquiring network; direct acquiring in 35+ markets | Good PayPal network coverage; weaker outside US/EU |

| Multi-Currency Settlement | 135+ currencies; automatic FX conversion; settlement in 25+ currencies | 150+ transaction currencies; multi-currency settlement accounts; better FX control for enterprises | 130+ currencies; settlement options limited compared to Adyen |

| Webhook Delivery Mechanics | HTTPS POST with HMAC-SHA256 signatures; event ordering not guaranteed; retry up to 3 days | HMAC-SHA256 signing; SOAP/REST; notification service with retry configuration | HMAC-SHA256; retry logic present but less configurable than Stripe |

| 3DS2 Support | Stripe Radar + 3DS2 natively; handles exemption logic | Full EMV 3DS2 with frictionless flow optimization | 3DS2 supported; less native exemption management |

| PCI Scope Reduction | Stripe.js / Payment Element keeps card data off your servers entirely | Client-side encryption library (CSE); similar scope reduction | Braintree.js / Drop-in UI; hosted fields approach |

| Radar / Fraud Tools | Stripe Radar with ML scoring; rule engine included | RevenueProtect with adaptive ML; stronger for enterprise volumes | Basic fraud tools; relies more on PayPal’s fraud network |

| Best Engineering Fit | Seed to Series B FinTechs; marketplaces; subscription SaaS | High-volume enterprise; global payment orchestration; regulated financial institutions | PayPal-native ecosystems; mobile commerce with existing PayPal user base |

Stripe is the right default for most FinTech startups — developer experience is the best in class, the documentation is genuinely excellent, and the Stripe Connect architecture handles marketplace split-payments cleanly. The FinTech development services model benefits from Stripe’s tight SDK ecosystem during rapid iteration phases.

Adyen becomes the correct choice when you’re processing high volumes across multiple geographic markets, need direct acquiring relationships, or require granular control over settlement currencies and interchange optimization. Its API is more verbose than Stripe’s, but the underlying network quality justifies the integration overhead at scale.

Braintree is defensible when your user base has high PayPal wallet penetration, or when you’re building in a market where PayPal’s local acquiring relationships are genuinely superior. Outside those scenarios, Stripe’s developer tooling and Adyen’s global reach are both stronger choices.

Deep Dive: Hardening the Integration

Idempotency Implementation

Idempotency is the single most important reliability concept in payment engineering. Without it, a network timeout between your server and the gateway leaves you in an ambiguous state: did the charge go through? If you retry naively, you risk double-charging the customer.

The correct pattern uses a client-generated idempotency key — a UUID tied to the specific payment intent — that you pass with every charge request. Stripe, Adyen, and Braintree all support idempotency keys at the API level. On the gateway side, if they receive two requests with the same key, they return the result of the first request rather than creating a second charge.

On your side, the implementation requires persistence. Here’s the production-grade flow:

- When a checkout session is created, generate a

payment_idempotency_key(UUID v4) and store it in your database tied to that order ID. - Acquire a distributed lock on that key before calling the gateway API. Redis

SET NX PX(set if not exists, with expiry) is the standard mechanism. - Call the gateway with the idempotency key in the request header.

- On success or a terminal failure, persist the result and release the lock.

- On network timeout, do NOT retry without the same idempotency key. Re-query using the key to determine actual state.

// Redis distributed lock (pseudocode)

lock_key = “payment_lock:” + idempotency_key

acquired = redis.SET(lock_key, process_id, NX=True, PX=30000)if not acquired:

// Another process holds the lock — poll for result or return 409

raise PaymentLockConflictExceptiontry:

result = gateway.charge(amount, currency, idempotency_key=idempotency_key)

persist_result(order_id, result)

finally:

redis.DEL(lock_key)

This eliminates the race condition where two concurrent requests (from a double-click, a retry, or a mobile app reconnect) attempt to charge the same order simultaneously.

Secure Webhook Processing

Webhooks are how gateways tell you what happened after the fact — charge succeeded, dispute opened, refund processed. They’re also the attack surface that most teams underestimate.

A robust webhook processing architecture has four components:

1. Signature Verification: Every gateway signs its webhook payloads using HMAC-SHA256. Verify the signature before processing anything. Stripe sends the signature in the Stripe-Signature header; compute the expected signature using your endpoint’s signing secret and reject any request where they don’t match. This prevents replay attacks and spoofed events.

2. Idempotent Event Processing: Webhooks can be delivered more than once. Your event processing must be idempotent. Store the event_id from the payload in a processed_webhook_events table. Before processing, check if the ID exists. If it does, return HTTP 200 immediately (to acknowledge receipt and stop retries) without re-executing business logic.

3. Out-of-Order Event Handling: Gateways don’t guarantee delivery order. A charge.refunded event can arrive before charge.succeeded. Design your state machine to handle this: use IF status != 'refunded' THEN update guards, or use event sequencing numbers if the gateway provides them. Never assume temporal ordering.

4. Dead-Letter Queue: Events that fail processing after N retries should land in a dead-letter queue (SQS DLQ, Kafka dead-letter topic) rather than being silently dropped. Alert on DLQ depth. These events represent real money movement that your system failed to record.

Retry policy for your own internal webhook processor should use exponential backoff with jitter: retry at 30s, 2m, 10m, 1h, 6h, 24h. After 24 hours with no success, route to DLQ and page on-call.

Tokenization and PCI Scope Reduction

PCI DSS Level 1 compliance is achievable by a startup team, but only if you architect correctly from day one. The fundamental principle: never let raw card data touch your servers. Use the gateway’s client-side JavaScript SDK (Stripe.js, Braintree.js, Adyen’s CSE library) to collect card data directly in the browser. The SDK tokenizes the card number before any data leaves the client, returning a single-use payment method token that your server exchanges for a charge.

Your backend receives only the token, never the PAN (Primary Account Number), CVV, or expiry in raw form. This removes your application servers, your database, and your network from PCI cardholder data environment scope — reducing your compliance surface area from hundreds of controls to a much smaller SAQ A or SAQ A-EP scope.

The architecture looks like this:

Browser → Stripe.js (collects card) → Stripe Servers (tokenizes) → Returns pm_token

Browser → Your Server (sends pm_token + order details)

Your Server → Stripe API (charges pm_token) → Returns charge result

Your Server → Database (records transaction, NOT card data)

Your database should store only: payment method token (masked), last 4 digits, card brand, expiry month/year, gateway customer ID. Never store raw card numbers, CVVs, or magnetic stripe data — doing so is a PCI violation regardless of encryption.

Internal links for compliance context: managed IT services for banking and the open banking API integration guide both cover adjacent regulatory considerations worth reviewing before your compliance audit.

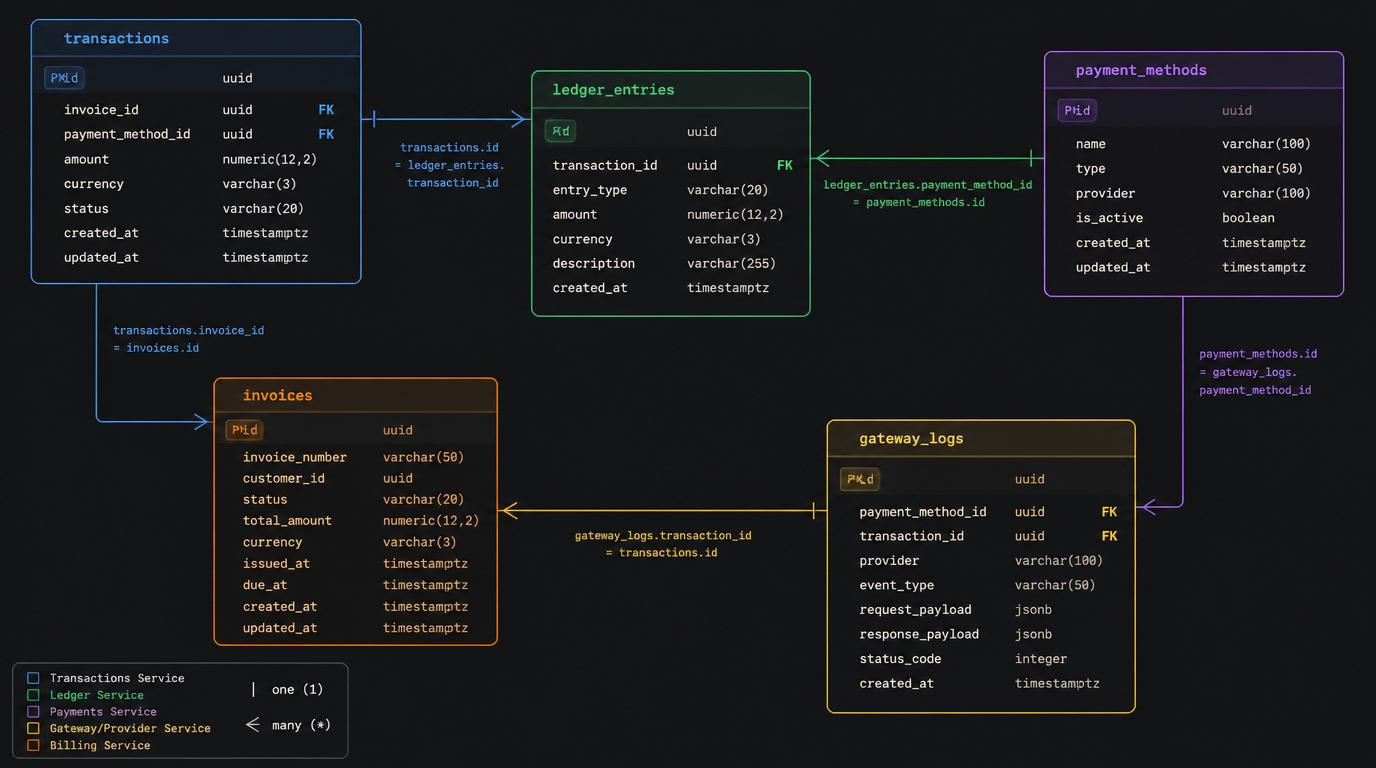

Database Schema and Transactional Integrity

Normalized Ledger Schema

Your database is the financial record of truth. It needs to be normalized, append-only where appropriate, and designed for auditability. Here’s a production-ready schema for the core tables:

— Core transaction record

CREATE TABLE transactions (

id UUID PRIMARY KEY DEFAULT gen_random_uuid(),

order_id UUID NOT NULL REFERENCES orders(id),

idempotency_key UUID NOT NULL UNIQUE,

gateway VARCHAR(50) NOT NULL, — ‘stripe’ | ‘adyen’ | ‘braintree’

gateway_txn_id VARCHAR(255) UNIQUE, — Gateway’s own reference

status VARCHAR(50) NOT NULL, — initiated | pending | succeeded | failed | refunded

amount BIGINT NOT NULL, — Always store in minor currency units (cents)

currency CHAR(3) NOT NULL, — ISO 4217

payment_method_id UUID REFERENCES payment_methods(id),

created_at TIMESTAMPTZ NOT NULL DEFAULT NOW(),

updated_at TIMESTAMPTZ NOT NULL DEFAULT NOW()

);— Double-entry ledger for financial accuracy

CREATE TABLE ledger_entries (

id UUID PRIMARY KEY DEFAULT gen_random_uuid(),

transaction_id UUID NOT NULL REFERENCES transactions(id),

account_id UUID NOT NULL REFERENCES accounts(id),

entry_type VARCHAR(10) NOT NULL, — ‘debit’ | ‘credit’

amount BIGINT NOT NULL,

currency CHAR(3) NOT NULL,

created_at TIMESTAMPTZ NOT NULL DEFAULT NOW()

);— Stored payment methods (tokens only, no raw card data)

CREATE TABLE payment_methods (

id UUID PRIMARY KEY DEFAULT gen_random_uuid(),

user_id UUID NOT NULL REFERENCES users(id),

gateway VARCHAR(50) NOT NULL,

gateway_token VARCHAR(255) NOT NULL, — pm_xxx or equivalent

card_last4 CHAR(4),

card_brand VARCHAR(20),

exp_month SMALLINT,

exp_year SMALLINT,

is_default BOOLEAN DEFAULT FALSE,

created_at TIMESTAMPTZ NOT NULL DEFAULT NOW()

);— Raw gateway event log for audit and reconciliation

CREATE TABLE gateway_logs (

id UUID PRIMARY KEY DEFAULT gen_random_uuid(),

event_id VARCHAR(255) UNIQUE NOT NULL, — Gateway event ID for deduplication

transaction_id UUID REFERENCES transactions(id),

event_type VARCHAR(100) NOT NULL,

payload JSONB NOT NULL,

processed_at TIMESTAMPTZ,

created_at TIMESTAMPTZ NOT NULL DEFAULT NOW()

);— Invoices

CREATE TABLE invoices (

id UUID PRIMARY KEY DEFAULT gen_random_uuid(),

user_id UUID NOT NULL REFERENCES users(id),

transaction_id UUID REFERENCES transactions(id),

amount BIGINT NOT NULL,

currency CHAR(3) NOT NULL,

status VARCHAR(50) NOT NULL, — draft | issued | paid | void

due_date DATE,

created_at TIMESTAMPTZ NOT NULL DEFAULT NOW()

);

Critical design decisions here: amounts are stored as BIGINT in minor currency units (2500 = $25.00) to avoid floating-point rounding errors. The idempotency_key column on transactions carries a UNIQUE constraint — your database enforces idempotency even if application-layer logic has a bug. gateway_logs stores the raw JSONB payload for complete auditability and reconciliation against gateway statements.

Preventing Race Conditions

In a distributed system processing concurrent payment events, two webhook deliveries for the same transaction can arrive simultaneously at two different pod instances. Without protection, both might attempt to update the transaction status, creating a race condition.

Use optimistic locking with a version column or SELECT FOR UPDATE SKIP LOCKED (PostgreSQL) to serialize access:

BEGIN;

SELECT id, status, version

FROM transactions

WHERE id = $1

FOR UPDATE;— Check current status before updating

UPDATE transactions

SET status = ‘succeeded’, version = version + 1, updated_at = NOW()

WHERE id = $1 AND version = $current_version;— If 0 rows updated, another process won the race — abort cleanly

COMMIT;

This atomic check-and-update prevents the status from being overwritten by a stale event.

Testing, Error Handling, and Edge Cases

Production payment systems fail in ways that unit tests don’t cover. Your pre-launch testing matrix needs to simulate failure modes explicitly.

Failure scenarios your test suite must cover:

- Network timeout mid-charge: Gateway connection drops after the charge is submitted but before response arrives. Verify that your idempotency key mechanism recovers correctly and doesn’t double-charge on retry.

- Gateway 500 error: Distinguish between a gateway error (charge may or may not have processed) and a network error (charge definitely didn’t reach the gateway). Your error classification logic determines retry safety.

- Partial refund race condition: Two refund requests arrive for the same transaction within milliseconds. Verify that database-level locking prevents over-refunding beyond the original amount.

- 3DS2 step-up authentication: The gateway returns a

payment_intent.requires_actionstatus requiring the user to complete a challenge. Your frontend must handle this redirect flow and your backend must poll or listen for the webhook confirming authentication completion before fulfilling the order. - Webhook out-of-order delivery: Simulate

charge.refundedarriving beforecharge.succeeded. Verify your state machine handles this without corrupting the transaction record. - Expired idempotency key: Test behavior when a Redis lock expires before the gateway responds. Verify re-query logic correctly determines charge state.

Engineering dashboard metrics to instrument from day one:

| Metric | Target | Alert Threshold |

|---|---|---|

| Payment success rate | > 97% | < 95% |

| Gateway API p99 latency | < 3s | > 5s |

| Webhook processing lag | < 30s | > 5 min |

| Idempotency key collision rate | < 0.01% | > 0.1% |

| DLQ depth | 0 | > 10 events |

| 3DS2 step-up conversion rate | > 85% | < 75% |

Use distributed tracing (OpenTelemetry with Jaeger or Datadog APM) to correlate payment requests end-to-end across your microservices. A single slow database query in the Ledger Service will show up clearly in your trace waterfall before a customer ever notices a slow checkout.

For custom software practices covering distributed system monitoring and AI-powered automation in FinTech, the same observability principles apply across the stack.

Conclusion: Production Readiness Checklist

The difference between a payment integration that works in staging and one that holds up in production under load, adversarial traffic, and regulatory scrutiny is architectural discipline applied consistently across every layer.

Before you go live with real card transactions, verify every item in this checklist:

Infrastructure & Architecture:

- Payment Service deployed in an isolated network segment with its own database

- No raw card data touches your application servers (Stripe.js / CSE library in use)

- Event bus (Kafka / SQS) decouples Payment Service from downstream consumers

- Outbox pattern implemented for reliable event publishing

Idempotency & Reliability:

- Idempotency keys generated at checkout session creation, stored in DB

- Redis distributed lock prevents concurrent duplicate charges

- Retry logic always uses original idempotency key, never generates a new one

- Gateway state re-query implemented for timeout recovery

Webhook Hardening:

- HMAC-SHA256 signature verification on every incoming webhook

-

event_iddeduplication table prevents double-processing - Out-of-order event handling in state machine logic

- Dead-letter queue configured with alerts on depth > 0

Database & Compliance:

- Amounts stored as BIGINT in minor currency units

-

UNIQUEconstraint onidempotency_keycolumn in transactions table -

SELECT FOR UPDATEor optimistic locking on concurrent updates -

gateway_logstable retaining raw JSONB payloads for 7+ years (regulatory requirement) - PCI DSS scope confirmed with QSA — SAQ A or SAQ A-EP level

- 3DS2 challenge flow tested end-to-end in sandbox

Observability:

- OpenTelemetry traces flowing through all payment services

- Dashboard tracking success rate, p99 latency, webhook lag, DLQ depth

- Alerting on all metrics against thresholds defined above

- On-call runbook for payment failure scenarios

Payment infrastructure built on these foundations can handle the transition from 100 transactions per day to 100,000 without architectural refactoring. The investment in correctness at the integration layer pays dividends every time a network partition doesn’t become a customer support ticket.

For teams that want to move faster without rebuilding this infrastructure from scratch, Genius Software’s custom software development services and FinTech expertise cover exactly this architecture — from gateway selection through PCI-compliant deployment.