Financial compliance has quietly crossed an inflection point. What used to be a quarterly reporting discipline managed by legal teams filling out PDFs has become an operational resilience challenge measured in milliseconds, data volumes, and cross-border regulatory simultaneity. A mid-sized FinTech processing 500,000 daily transactions now faces concurrent obligations under FinCEN’s AML program rules, the EU’s actively enforced DORA framework, SEC reporting requirements, and evolving FATF recommendations — each with distinct data models, reporting cadences, and audit expectations. The engineering teams responsible for staying compliant are no longer just compliance-adjacent; they are building distributed systems that must be as reliable as the financial rails they sit alongside.

This guide delivers a scalable architectural blueprint for RegTech platform development that meets 2026 enterprise standards — not as theory, but as implementable system design. We will work through microservices isolation for KYC and AML boundaries, zero-trust data infrastructure, Agentic AI pipelines for Automated Regulatory Intelligence, real-time Kafka-based transaction monitoring, and the immutable audit log architecture that makes your platform defensible under examination. By the end, you will have the engineering vocabulary and system design clarity to build compliance infrastructure that auditors can verify and regulators can trust.

The Architecture of Modern RegTech: Modular, Resilient, and Isolated

Microservices Isolation for Compliance Domains

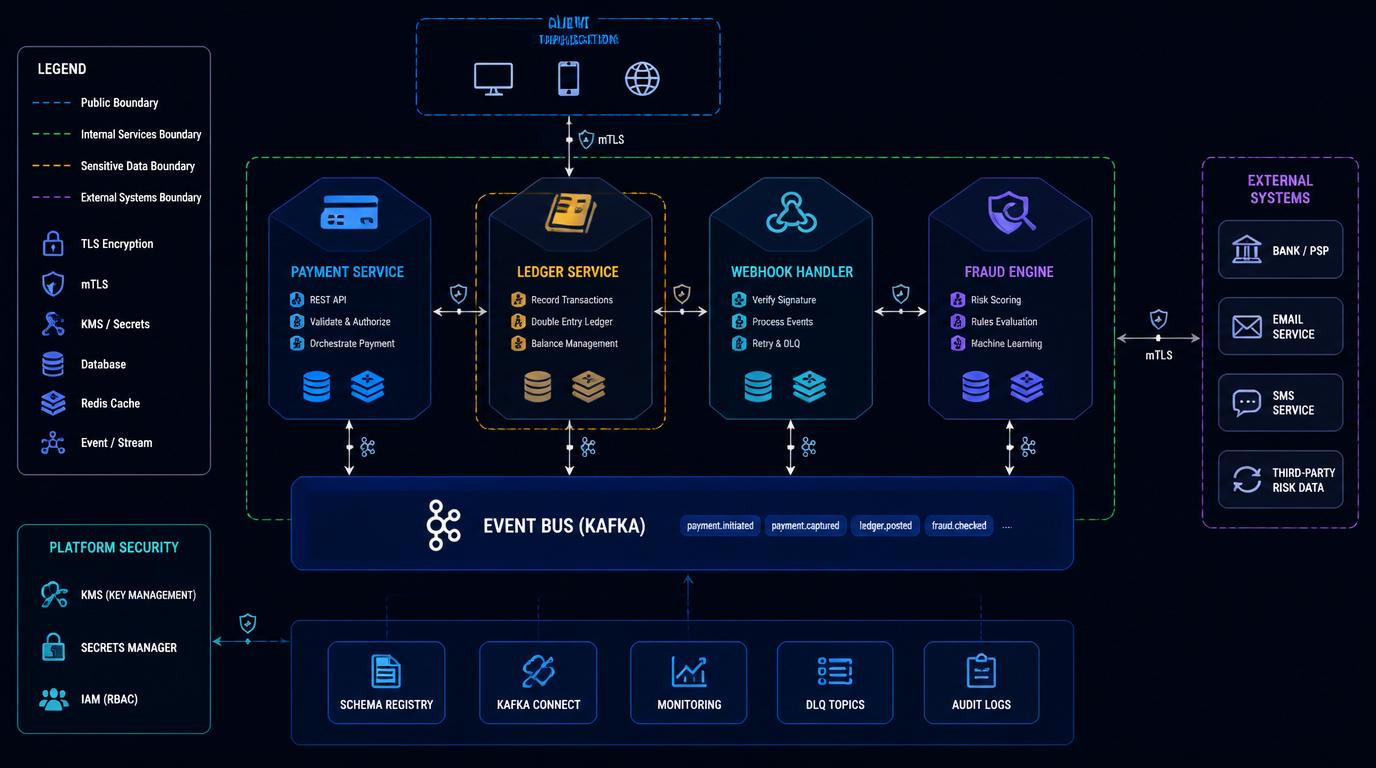

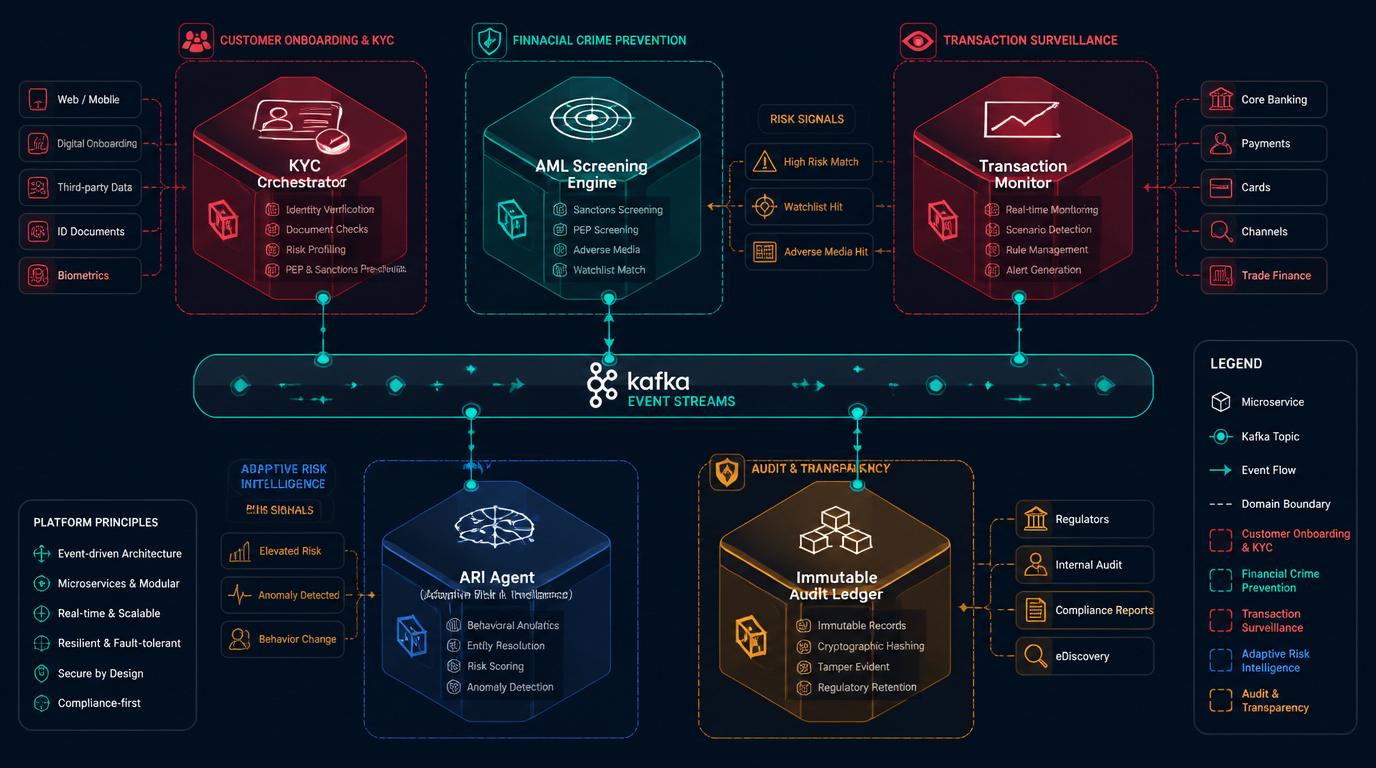

The foundational architectural principle in RegTech platform engineering is that compliance domains must map one-to-one with service boundaries. This is not a generic microservices recommendation — it is a regulatory necessity. KYC identity data, AML screening results, transaction monitoring signals, and case management records each carry distinct data sensitivity classifications, retention requirements, and access control obligations. Commingling them in a shared data store is both an operational risk and a compliance liability.

A production-grade RegTech architecture isolates these bounded contexts into independently deployable, independently auditable services:

- Identity Verification Service (IVS) — Orchestrates multi-vendor KYC workflows: document verification (Jumio, Onfido, or in-house OCR pipelines), biometric liveness detection, and PEP/sanctions pre-screening. Owns its own encrypted identity data store. Access is API-only, with all reads logged to the immutable audit ledger.

- AML Screening Engine — Performs name-matching against OFAC, UN, EU Consolidated List, and HMT sanctions databases. Runs entity resolution across multilingual name variants. Maintains its own screening result history, never mutating prior records — only appending new screening events.

- Transaction Monitoring Service (TMS) — Consumes real-time payment event streams, applies rule-based and ML-based anomaly detection, and publishes risk-scored events downstream. Stateless computation layer; state lives in the event log.

- Regulatory Reporting Engine — Generates jurisdiction-specific reports (FinCEN SAR/CTR, EU DORA incident reports, SEC Form PF, FATCA/CRS XML filings). Pulls from the event log, never from transactional operational databases — ensuring reporting never degrades transaction processing performance.

- Case Management Service — Manages the full lifecycle of flagged entities and transactions from initial alert through investigation, decision, and regulatory filing. Immutable append-only case history. Evidence attachments stored in WORM-compliant object storage.

- Automated Regulatory Intelligence (ARI) Agent — Monitors global regulatory bodies for rule changes, parses and classifies updates, and pushes structured change proposals to compliance officers for human review. Covered in depth in the next section.

Each service deploys with its own database cluster. Cross-service communication uses an internal event bus — Apache Kafka is the standard choice — rather than synchronous HTTP calls between compliance-sensitive services. This eliminates the failure cascade risk where a degraded reporting engine delays transaction screening.

Zero-Trust Infrastructure for Cross-Border Data Processing

Financial institutions operating across jurisdictions face a data sovereignty problem that architecture must solve before compliance can. GDPR in the EU, PDPA in Southeast Asia, and data localization requirements in markets like Brazil (LGPD) and India mandate that certain categories of personal financial data cannot transit or rest in specific geographic regions.

Zero-trust network architecture addresses the access control dimension of this problem. In a zero-trust RegTech deployment, no service is implicitly trusted by virtue of its network location. Every inter-service call carries a short-lived mTLS certificate and a JWT carrying the requesting service’s identity and permitted scopes. Policy enforcement happens at the sidecar proxy layer (Envoy, with Open Policy Agent handling authorization decisions), not at the application layer.

For cross-border data flows, this translates into a data residency routing layer that sits ahead of the KYC and AML services. Incoming identity data is tagged with its jurisdiction of origin at ingestion. The routing layer enforces that EU-origin personal data is processed only by service replicas running in EU-region infrastructure, with audit trails confirming regional confinement. This architectural pattern satisfies data localization requirements without requiring a separate compliance codebase per jurisdiction.

Designing for DORA Enforcement

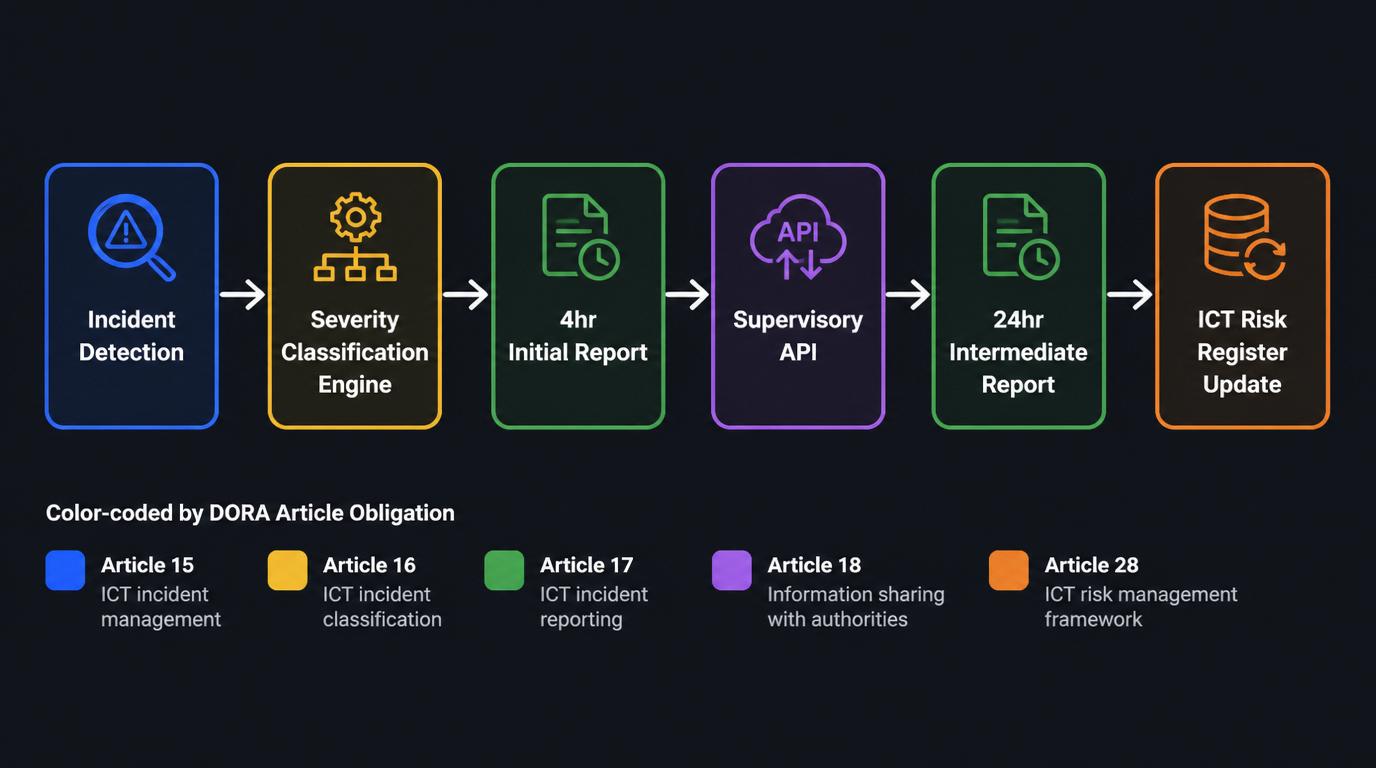

The EU’s Digital Operational Resilience Act entered active enforcement in January 2025. DORA imposes legally binding ICT risk management requirements on financial entities operating in the EU — covering incident classification, recovery time objectives, third-party ICT risk management, and mandatory reporting of major operational incidents to financial supervisors within strict timelines.

Engineering for DORA means several concrete architectural choices:

ICT Risk Register as a Living Data Model: DORA Article 6 requires a maintained, comprehensive ICT risk register. This should be a first-class database entity in your RegTech platform — not a spreadsheet. Model ICT assets, their criticality classification, their dependency graph, and their associated risk assessments as structured records that can be queried, version-controlled, and exported for supervisory review.

Incident Detection and Reporting Pipelines: DORA requires classification of ICT incidents by impact severity and mandates reporting of major incidents to competent authorities within 4 hours (initial report) and 24 hours (intermediate report). Your monitoring infrastructure must produce structured incident records that your Regulatory Reporting Engine can translate into jurisdiction-specific supervisory notification formats automatically.

Third-Party ICT Risk: If your RegTech stack depends on cloud infrastructure providers, SaaS screening databases, or AI model providers, DORA requires you to maintain contractual exit strategies and demonstrate operational substitutability. Document this dependency mapping in your ICT Risk Register. Your managed IT services architecture strategy needs to account for concentration risk across cloud providers.

Automated Regulatory Intelligence: Injecting AI into the Compliance Pipeline

Moving Past Manual Regulatory Monitoring

Compliance teams at most financial institutions still discover regulatory changes through manual processes — newsletter subscriptions, legal counsel alerts, or regulatory body websites checked periodically. This approach is structurally incompatible with the pace of rule change in 2026. The SEC issued over 40 significant rule amendments in 2024. FinCEN’s AML program rules are actively evolving under the Corporate Transparency Act implementation. The EU is producing implementing technical standards under DORA on a rolling basis. No legal team reads fast enough.

Automated Regulatory Intelligence (ARI) replaces this manual process with an agentic AI pipeline that continuously monitors, parses, classifies, and structures regulatory updates across your relevant jurisdictions.

The ARI pipeline architecture consists of four layers:

1. Ingestion Layer: Headless browser agents and structured API clients scrape and ingest content from regulatory sources: SEC EDGAR, FinCEN regulatory releases, EU Official Journal, FCA Policy Statements, FATF publications. Raw content is stored as immutable documents with source URL, ingestion timestamp, and hash fingerprint for auditability.

2. Classification and Extraction Layer: A fine-tuned LLM (a domain-adapted model built on a Llama 3 or Mistral base, or a hosted frontier model with strict data handling agreements) processes ingested regulatory documents. The model is prompted to extract structured metadata: regulatory body, applicable jurisdiction, effective date, affected compliance domains (KYC, AML, reporting, data residency), and a plain-language summary of the required operational change.

The prompt engineering here requires careful guardrails. Regulatory AI cannot hallucinate. The system prompt must enforce that the model cite specific document sections for every claim it extracts, output a confidence score for each extraction, and flag any ambiguous language for human review rather than attempting to resolve it autonomously. Output schema is validated against a JSON Schema definition before any downstream propagation.

3. Human-in-the-Loop (HITL) Review Workflow: Extracted regulatory change proposals flow into a case management queue where a compliance officer reviews, confirms, or corrects the AI’s classification. Only HITL-approved records are promoted to the policy database. This is non-negotiable — no AI-generated regulatory interpretation should modify a production compliance rule without human sign-off. The HITL workflow itself generates an audit record: who reviewed, what they approved, when, and any modifications they made.

4. Policy Propagation Layer: Approved regulatory changes trigger structured policy update events on the internal event bus. Downstream services — the AML Screening Engine, Transaction Monitoring Service, Regulatory Reporting Engine — subscribe to policy update events and reload their rule configurations without requiring a code deployment. This is the critical architectural advantage of event-driven compliance rule management: your screening logic can update to reflect a new sanctions list addition within minutes of regulatory publication, not at the next deployment cycle.

The Agentic AI in 2025 analysis and Genius Software’s AI development practice both expand on multi-agent orchestration patterns that apply directly to ARI pipeline design.

Hallucination Mitigation in Legal AI

The failure mode unique to LLM-based regulatory parsing is confident wrongness. A model that extracts an incorrect effective date for a compliance deadline, or misclassifies a rule as applying to payment processors when it applies only to broker-dealers, creates downstream liability. Mitigation strategies that must be implemented at the architecture level:

- Retrieval-Augmented Generation (RAG): Ground every LLM extraction in the specific source document. Use a vector database (Pinecone, Weaviate, or pgvector) to retrieve the relevant document chunks and include them verbatim in the model’s context. This constrains the model to what is actually written.

- Confidence thresholding: Any extraction with confidence below a defined threshold (typically 0.80 for regulatory AI) routes directly to HITL queue without being presented as a candidate for auto-approval.

- Contradiction detection: A secondary validation pass checks extracted metadata against existing policy records and flags contradictions (e.g., a new rule with an effective date predating a prior rule covering the same domain) for human investigation.

Data Engineering for KYC/AML Orchestration and Transaction Monitoring

Real-Time Transaction Ingestion

The core data engineering challenge in AML transaction monitoring is throughput with latency constraints. A financial institution processing 500,000 daily transactions needs each one screened against sanctions lists, behavioral baselines, and peer-group anomaly models in near-real time — typically within 200–500 milliseconds — without blocking the payment execution path.

Apache Kafka is the standard infrastructure choice for this requirement. The transaction processing system publishes payment events to a Kafka topic at the moment of authorization. The Transaction Monitoring Service consumes from this topic in parallel, applying screening logic asynchronously. Risk scores and any alerts are published to a downstream topic. The payment execution path is never blocked by screening latency; instead, a post-authorization monitoring pattern flags suspicious transactions for review while allowing low-risk payments to settle.

The streaming architecture for the Transaction Monitoring Service:

[Payment Gateway / Core Banking]

→ Kafka Topic: raw.transactions

→ TMS Consumer Group (partitioned by account_id for ordering)

→ Sanctions Screening Module (real-time OFAC/UN lookup via in-memory Bloom filter + authoritative DB check)

→ Behavioral Anomaly Module (Flink stateful stream processing, maintains rolling 30/90/180-day behavioral windows)

→ Velocity Rules Engine (Redis-backed counter store: transaction count / amount by entity / time window)

→ Kafka Topic: risk.scored.transactions

→ Alert Routing Service (thresholds → Case Management Service)

→ Kafka Topic: monitoring.audit.log (all screening decisions, immutable)

The in-memory Bloom filter for sanctions screening deserves specific attention. A full database lookup for every transaction is too slow under load. A Bloom filter loaded from the consolidated sanctions lists (OFAC SDN, UN, EU) serves as a probabilistic first-pass gate in microseconds. Transactions where the entity name produces a positive Bloom filter result (acknowledging the acceptable false-positive rate) are then routed to an authoritative database lookup. Transactions that don’t match the Bloom filter at all clear the sanctions check without a database round-trip.

Reducing False Positives with ML Entity Resolution

AML false positives are an expensive operational problem. Screening “Mohamed Al-Hassan” against a sanctions list containing “Muhammad Al-Hasan” requires more than string equality — it requires multilingual name normalization, phonetic matching (Metaphone, Soundex, or custom transliteration models), and entity resolution that understands that the same person can appear in corporate ownership structures under multiple name variants across multiple jurisdictions.

The entity resolution pipeline for high-quality AML screening combines:

- Transliteration normalization: Arabic, Cyrillic, Chinese, and other non-Latin scripts transliterated to Latin equivalents using Unicode CLDR data before matching. Critical for international sanctions list coverage.

- Phonetic matching: Metaphone3 or a custom learned phonetic embedding model for name-sound similarity scoring.

- Graph-based ownership resolution: Legal entity ownership webs — shell company chains, beneficial ownership structures — modeled as directed graphs in a graph database (Neo4j). AML screening traverses the ownership graph to identify sanctioned beneficial owners even when they are several corporate layers removed.

- ML scoring model: A trained binary classifier (XGBoost or a fine-tuned transformer) takes the combined signals (name similarity score, jurisdiction match, transaction context, historical behavior) and outputs a match probability. Alerts are only generated when this probability exceeds a configurable threshold.

This architecture can reduce false positive rates by 60–75% compared to pure rule-based string matching — directly translating into fewer investigator hours per 1,000 transactions.

ETL Pipeline Design for Compliance Data Warehousing

The reporting and analytics layer of a RegTech platform requires a purpose-designed ETL architecture that separates compliance reporting workloads from operational transaction processing completely. Running regulatory reports against your operational databases creates contention that degrades payment processing performance — an unacceptable coupling.

The recommended pattern:

- Operational databases (Postgres, Oracle) serve transaction processing exclusively.

- Change Data Capture (CDC) via Debezium streams operational changes into Kafka in real time.

- A streaming ETL layer (Apache Flink or Spark Structured Streaming) transforms, enriches, and aggregates these events into compliance-ready data models.

- The output lands in a secure data lake — S3 or Azure Data Lake Storage with server-side encryption, object-level access logging, and WORM (Write Once Read Many) retention locks applied at the bucket/container policy level.

- Reporting queries run against the data lake or a downstream columnar analytical store (Amazon Redshift, Snowflake, or ClickHouse for high-concurrency reporting).

WORM storage is not optional for regulatory compliance. Both SEC Rule 17a-4 and FINRA Rule 4370 mandate that compliance records be stored in non-rewriteable, non-erasable format for defined retention periods (typically 6–7 years for AML records). Your object storage policy must enforce object immutability at the infrastructure level — not as an application-layer convention.

Immutable Audit Infrastructure and Cryptographic Ledger Integrity

Every action taken by every service in a RegTech platform must produce an audit record that cannot be modified after the fact. This is not a logging recommendation — it is a legal requirement across virtually every financial compliance framework. The audit log is the artifact a regulator examines during an examination. Its integrity is your compliance defensibility.

Audit Log Architecture Requirements:

| Property | Implementation |

|---|---|

| Immutability | WORM-locked object storage; append-only database tables with INSERT-only grants |

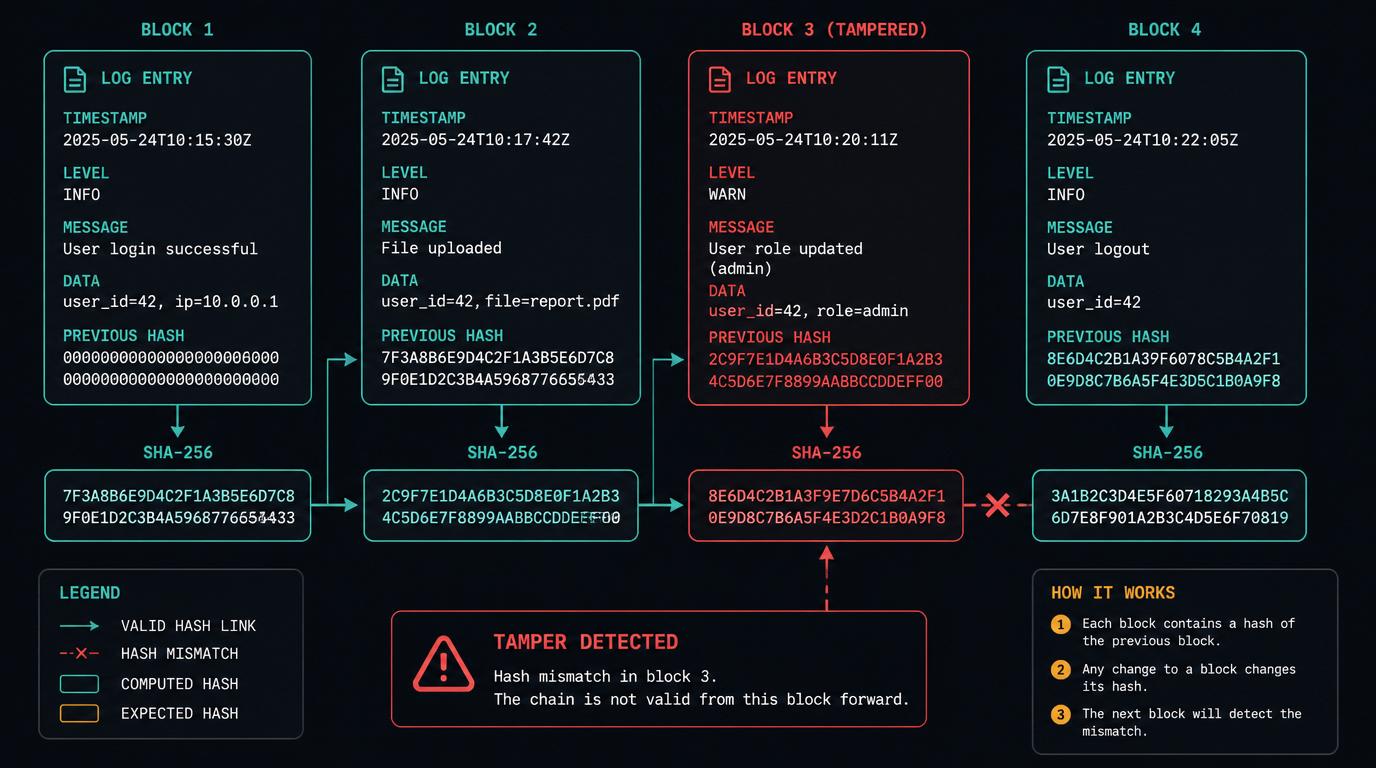

| Integrity verification | SHA-256 hash chaining: each log entry’s hash includes the hash of the prior entry, creating a tamper-evident chain |

| Completeness | All service-to-service API calls, all data access events, all human actions logged at the middleware layer — not at the application layer |

| Availability | Multi-region replication; audit logs must survive the failure of any single infrastructure component |

| Searchability | Structured JSON log format; indexed in Elasticsearch or OpenSearch for investigator search workflows |

| Retention enforcement | Automated lifecycle policies enforcing minimum retention and flagging premature deletion attempts |

Hash chaining deserves elaboration. Each audit log entry contains a previous_hash field that stores the SHA-256 hash of the immediately preceding entry. A verification process can traverse the chain and confirm no entry has been inserted, modified, or deleted. This is the same cryptographic principle underlying blockchain ledgers, implemented without the overhead of a distributed consensus protocol — a centralized hash chain is sufficient for most regulatory audit requirements and is far simpler to operate.

For case management records specifically, all evidence attachments (transaction records, KYC documents, screening results, investigator notes, SAR filing copies) should be stored in WORM object storage with a cryptographic content hash stored in the case management database. Before any regulatory submission that references these attachments, the system recomputes the content hash and verifies it against the stored value — confirming the evidence has not been tampered with since it was collected.

Cross-Border Jurisdiction Reporting Engine

Financial institutions with multi-jurisdiction footprints face a reporting multiplicity problem. A transaction that triggers a Currency Transaction Report (CTR) obligation in the US may simultaneously trigger a FATCA report (if a US person is involved), a Suspicious Activity Report to FinCEN, and a notification to the relevant EU competent authority under DORA if the transaction involved an EU-regulated entity. Each report has a different format, a different submission endpoint, and a different deadline.

The Regulatory Reporting Engine solves this through a report orchestration pattern built on these components:

Jurisdiction-Obligation Mapping Table: A database table that maps transaction attributes (jurisdiction of parties, transaction type, amount thresholds, entity types) to reportable obligations. This table is maintained by the ARI pipeline — when a regulatory change affects reporting thresholds, the ARI agent updates this mapping after HITL approval, without a code release.

Report Generation Templates: Jurisdiction-specific report templates defined as declarative configurations (JSON or YAML), not hardcoded logic. A FinCEN SAR template defines the XML schema, field mappings from internal data models, and the submission endpoint. Adding a new jurisdiction means adding a template, not writing code.

Submission Orchestrator: Manages the full submission lifecycle — template rendering, digital signature (required for several jurisdictions), submission to regulatory API, acknowledgement receipt, retry on failure, and status tracking. All submission events are recorded in the audit log.

Deadline Management: A scheduler monitors pending reporting obligations and their statutory deadlines. CTRs are due within 15 days of the triggering transaction. DORA major incident initial reports are due within 4 hours. The scheduler alerts compliance officers as deadlines approach and auto-escalates overdue obligations.

This pattern allows the same core engineering codebase to serve regulatory reporting across the US, EU, UK, Singapore, and UAE without jurisdiction-specific branches in the application logic. The configuration layer absorbs the variation.

For teams building on custom software development foundations, Genius Software’s FinTech software expertise covers the full stack from data engineering through regulatory API integration.

Production Readiness: RegTech Engineering Checklist

Building a RegTech platform that survives regulatory examination and operates reliably under production load requires discipline across infrastructure, data, AI, and process layers. This checklist consolidates the architectural requirements from every section above:

Architecture and Service Isolation:

- Each compliance domain (KYC, AML, TMS, Reporting, Case Management) deployed as an isolated service with its own database

- Zero-trust mTLS between all services; OPA policy enforcement at the sidecar layer

- Data residency routing enforced at the infrastructure layer for cross-border personal data

- DORA ICT Risk Register implemented as a first-class database entity

- Third-party ICT dependency map maintained and exit strategies documented

ARI Pipeline:

- Regulatory source ingestion agents deployed for all relevant jurisdictions

- LLM extraction layer with RAG grounding, confidence thresholding, and contradiction detection

- HITL review workflow with full audit trail for every human decision

- Event-driven policy propagation to downstream compliance services

KYC/AML Data Engineering:

- Kafka-based real-time transaction ingestion with partitioning by account entity

- Bloom filter + authoritative DB two-pass sanctions screening implemented

- ML entity resolution covering transliteration, phonetic matching, and ownership graph traversal

- CDC pipeline feeding compliance data lake; WORM retention locks enforced at storage level

- Behavioral baseline windows (30/90/180-day) maintained in Flink stateful stream processor

Audit and Integrity:

- SHA-256 hash chaining across all audit log entries; verification process scheduled and alerting on chain breaks

- Case management evidence stored in WORM object storage with content hash verification before each regulatory submission

- All inter-service API calls and human actions logged at middleware layer, not application layer

- Multi-region replication for audit log storage

Reporting and DORA:

- Jurisdiction-obligation mapping table driving report generation (no hardcoded jurisdiction logic)

- Declarative report templates for all active jurisdictions; new jurisdictions added via configuration

- Submission orchestrator with retry, acknowledgement receipt, and status tracking

- DORA incident classification and 4-hour/24-hour report generation pipeline in place

- Deadline management scheduler with escalation for overdue obligations

The financial institutions that navigate the next generation of regulatory complexity without operational disruption will be those that built their compliance infrastructure as a first-class engineering discipline — not as an afterthought patched onto a core banking system. RegTech done correctly is a competitive advantage: faster time to market in new jurisdictions, lower compliance operational costs, and a demonstrably defensible position when regulators come examining.